Macro Flash Report

Housing Sales & Prices

Takeaway:

Additional August housing data highlight the continued rebalancing within the new and existing home sectors. As expected, inventories are starting to increase alongside the lower trend in mortgage rates, however, buyers appear to be temporarily waiting to see just how low rates will go.

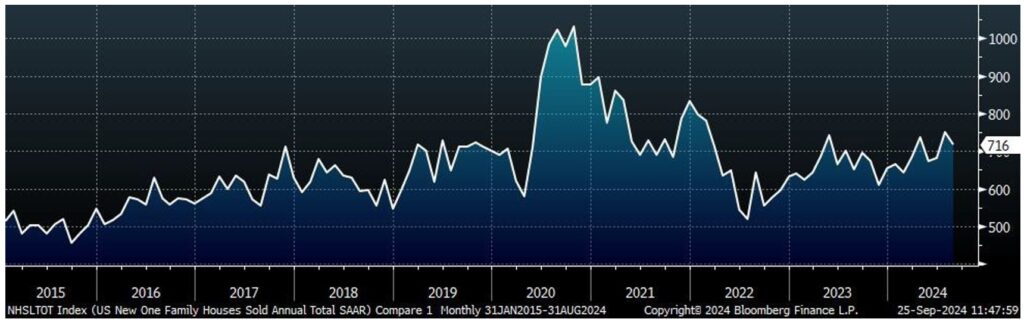

New Home Sales

In August, New Home Sales declined by -4.7% to a seasonally adjusted annual rate of 716k units. This drop follows a significant 10.3% increase in July but still slightly surpassed market expectations of 699k.

Existing Home Sales also fell, decreasing by -2.5% to an annualized rate of 3.86m units, down from a revised higher 3.96m in July and missing the forecasted 3.90m sales. This marks the fourth decline this year, despite a decrease in mortgage rates during the period.

- The median price of existing homes dropped by $10,200 to $416,900.

- The inventory of unsold homes rose slightly, reaching the equivalent of 3.9 months of sales at the current pace, up from 3.6 months in the previous month.

MBA Mortgage Applications surged by 11% in the week ending September 20th, building on a 14.2% increase from the prior week. The rise pushed application volumes to their highest level since June 2022.

The uptick in mortgage demand coincides with a continued decline in benchmark mortgage rates, with the MBA 30-Year Mortgage Rate falling to a two-year low of 6.13%, driven by expectations of a dovish stance from the Fed that kept long- term Treasury yields subdued. This marked the eighth consecutive week of declining rates, accumulating a total decrease of 69 basis points.

Additionally, the MBA Refinance Applications, which are particularly sensitive to short-term rate changes, jumped by 20% week-over-week.

In July, the S&P CoreLogic Case-Shiller 20-City Home Price Index increased by 5.9% YoY, down from the 6.5% rise in June and closely aligning with the anticipated 5.8%. This represents the slowest growth rate since November 2023, highlighting the dampening effect of higher interest rates on housing demand. Despite the slowdown, July marked the ninth consecutive month of price growth above 5%. Month-over-month, the index was unchanged, ending a streak of four consecutive monthly increase.