Fundamental Report

Supply Side Takeaway:

The new October estimate for imports remains elevated but brings the expected level more in line with recent months rather than implying a renewed surge, and the domestic–global HRC spread contracted slightly on the week.

This week’s data: The Domestic – Global HRC price differential tightened further this week as the domestic spot price remained unchanged while the global average price increased slightly. On the imports side, this week’s estimate for October arrivals indicates a jump up from September’s census figure, which came in at the lowest level since June. Domestic production ticked up further, however, remains at subdued levels.

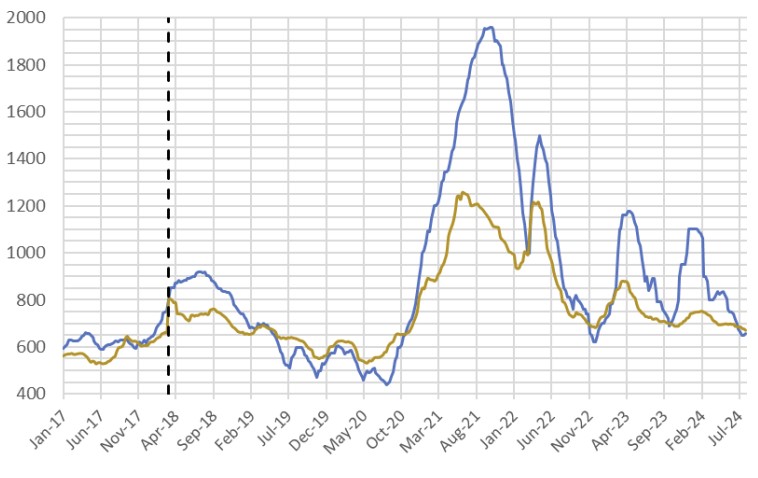

HRC Spot Prices – US Domestic & Global

HRC Spot Prices – US Domestic & Global

- The global HRC spot price rose to $652 from $650. This week the price changes were from: +$17 in Europe, -$2 in Korea, and -$2 in China.

- The Domestic – Global HRC spread contracted further, narrowing to $57.73 from $59.98.

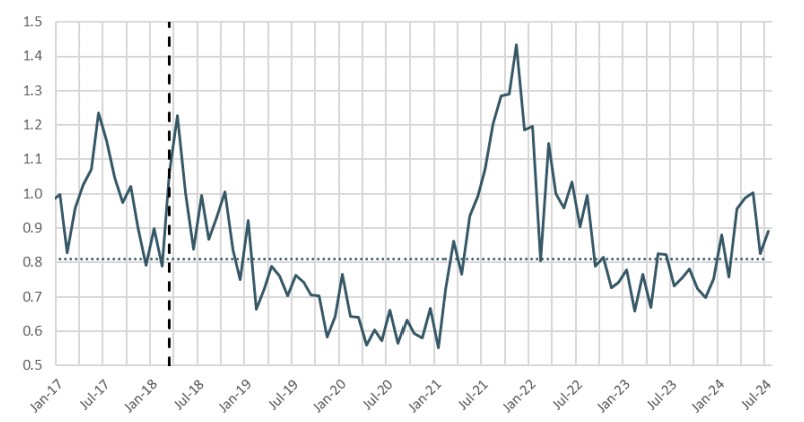

Total Sheet Imports (s.ton)

Total Sheet Imports (s.ton)

- This week’s imports estimated sheet arrivals for October indicate an increase, rising to 912k tons from September’s census figure of 841k.

- The named countries from the filed trade petition represent nearly 80% of the expected total arrivals for coated products in 2024.

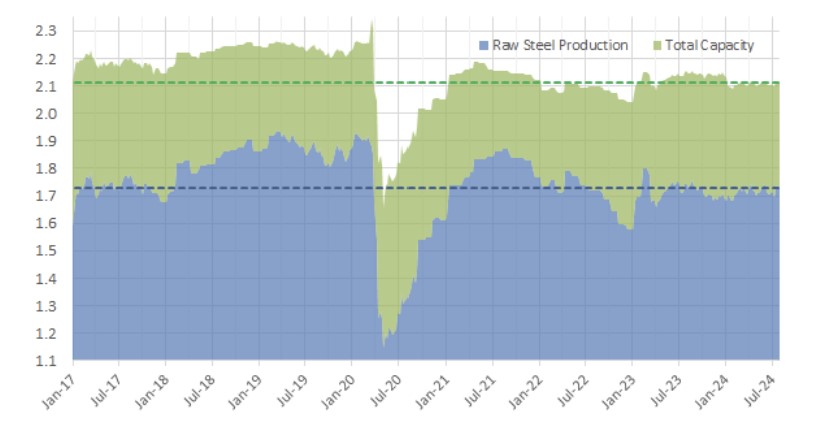

Domestic Production (s.ton)

Domestic Production (s.ton)

- For the week ending on October 26th, capacity utilization ticked up by 1.3% to 74.7% and domestic raw steel production rose to 1.660m from 1.631m/tpw.

- This brings the year-to-date production to 72.729m, operating at a rate of 764%, -1.7% below this point last year.