RESEARCH AND ANALYSIS

2024 REVIEW & 2025 OUTLOOK

JANUARY 6, 2025

Major Takeaways:

Overall, the U.S. economy is in a good position to continue to be the envy of the rest of the developed market economies.

Balance sheets for both consumers and firms are in a healthy position which should lead to stable growth and a higher probability of reacceleration than cooling.

1Q25 is set up to have strong headwinds as last year’s steel surplus still exists. Dynamics in 4Q24 domestic production and buyer inventories suggest that a rally in HRC prices would be muted and find resistance at $800.

We are already seeing signs of life in steel demand. However, 2Q25 and beyond is the timeframe where we anticipate strong recoveries in all the steel demand subsectors that we measure, excluding automotive. That is construction, manufacturing, appliance/household, and energy.

Overall, the U.S. economy is in a good position to continue to be the envy of the rest of the developed market economies.

Balance sheets for both consumers and firms are in a healthy position which should lead to stable growth and a higher probability of reacceleration than cooling.

1Q25 is set up to have strong headwinds as last year’s steel surplus still exists. Dynamics in 4Q24 domestic production and buyer inventories suggest that a rally in HRC prices would be muted and find resistance at $800.

We are already seeing signs of life in steel demand. However, 2Q25 and beyond is the timeframe where we anticipate strong recoveries in all the steel demand subsectors that we measure, excluding automotive. That is construction, manufacturing, appliance/household, and energy.

Latest

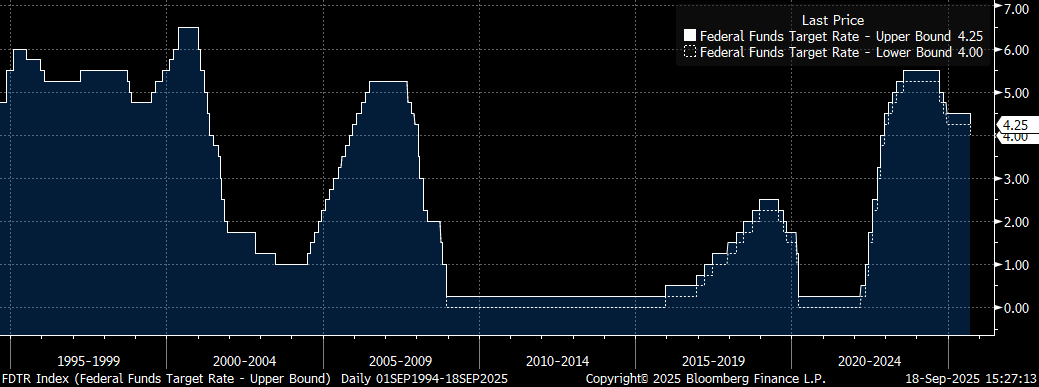

Sep 18, 2025

FED CUTS RATES FOR THE FIRST TIME IN 2025

The Federal Open Market Committee lowered the policy rate 25 basis points to 4.00-4.25% on Wednesday, its first cut of the year.

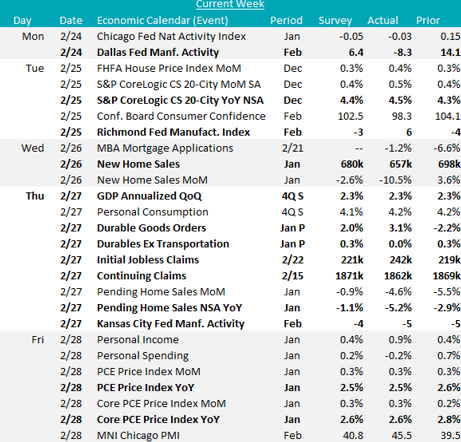

Feb 28, 2025

Macro Report

Manufacturing activity has come in below expectations, but shows stead growth, while housing sales data disappointed to start the year.

Feb 27, 2025

Macro Flash Report

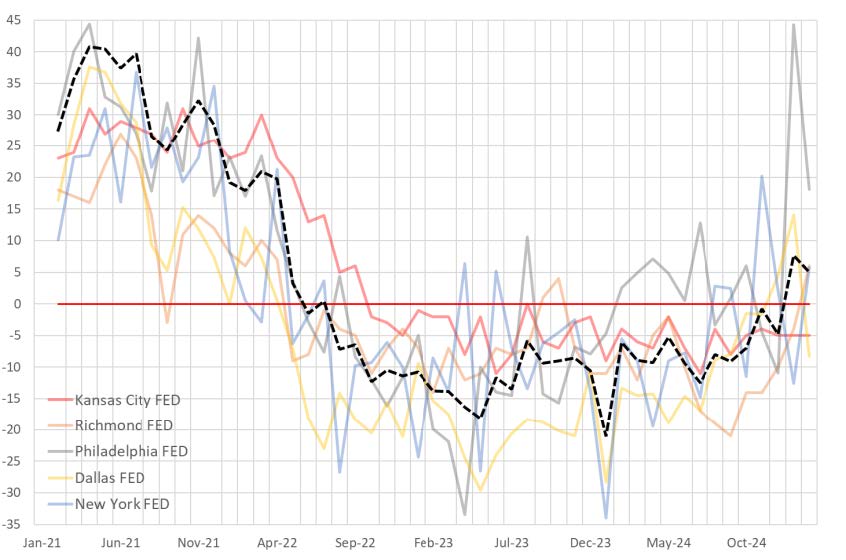

Although the recovery in manufacturing has been slower than some expected, underlying dynamics suggest that we are on track for sustained expansion for the first half of 2025. Fed Manufacturing Survey data point to another expansionary print in the ISM Manufacturing PMI, due out on Monday, March 3rd.

Feb 26, 2025

Macro Flash Report

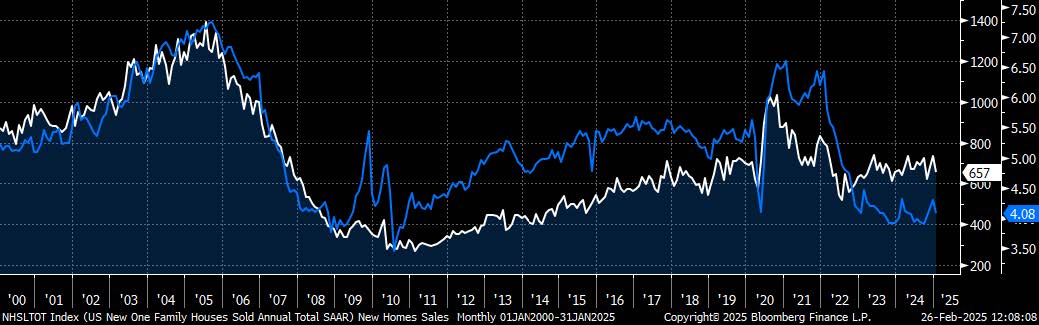

Similar to the impact on housing starts, January’s unusually severe winter storms dragged down sales of both new and existing homes. Still elevated mortgage rates and increasing prices will likely stand in the way a surge in sales, but “too-low” existing home inventories will keep the floor for new home sales elevated.

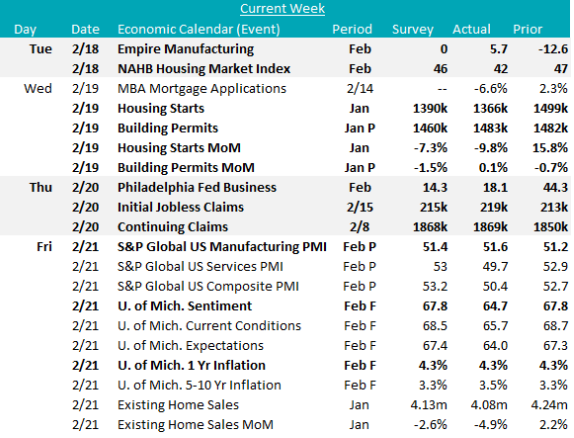

Feb 21, 2025

Macro Report

This week provided further encouraging data on the rebound in manufacturing, while an especially cold January froze out housing activity. Consumer concerns around upcoming inflation continue to accelerate.

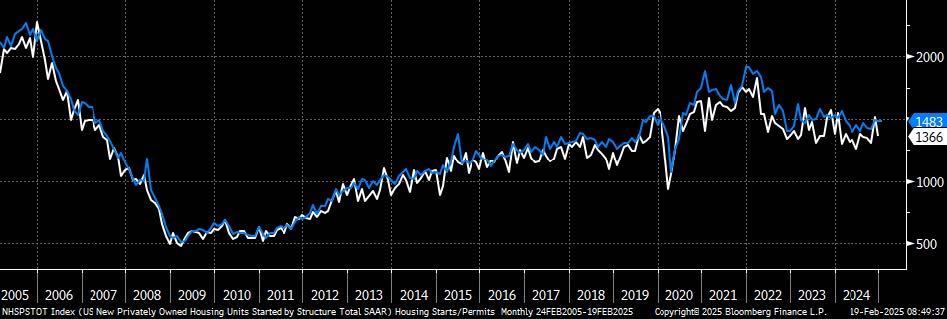

Feb 19, 2025

Macro Flash Report

January weather clearly impacted the housing data, with a worse than expected decline in starts. Permits remain in a healthy position and suggest continued activity in new residential construction in 2025.

More Reports

Show More Reports