Macro Report

Week’s Takeaway:

This week’s data was heavy on price pressure and inflation and light on updates to industrials. While the FOMC is all but guaranteed to vote for an interest rate cut in next week’s meeting, the more important signal will come for next year’s change in the SEP (Summary of Economic Projections).

Notes:

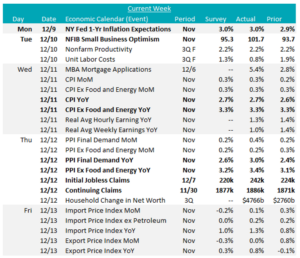

In November, the NFIB Small Business Optimism soared to 101.7, coming in above the 50-year average of 98 for the first time in 34 months and reaching the highest level since June 2021. This follows a 93.7 reading in October and exceeded expectations of an increase to 94.6. Additionally, the Uncertainty Index dropped by 12 points to 98 as future business conditions become clearer following the election.

Both Topline and Core CPI (Consumer Price Index) rose 0.3% MoM, which is slightly higher than expected. This led to YoY increase to 2.7% and 3.3%, respectively. PPI (Producer Price Index) came in hotter – Topline and Core PPI were up 3% and 3.4% YoY, respectively, both beating expectations. While many have pointed to the anomaly of surging egg prices as a “one off” for the November Topline PPI, the fact remains that Core PPI (ex. Food & Energy) has been in a slow structural uptrend since last December. Finally, the November NY Fed 1yr-Inflation Expectations were in line with expectations at 3%. This was up from 2.9% in October.

Next Week’s Notes:

Next week a range of data for key steel-consuming sectors will be released, alongside a Fed rate cut decision and macroeconomic indicators.

In manufacturing, the first three December Fed Manufacturing Surveys will be issued, with the NY Empire index expected to ease to 6.6 from 31.2 and the Philadelphia index is anticipated to improve to 2.4 from -5.5. The Kansas City index will also be released. Additionally, the preliminary December S&P Global US Manufacturing PMI will be reported.

November’s Industrial Production is forecasted to rise by 0.2%, with

Capacity Utilization expected to tick up to 77.3% from 77.1%. Manufacturing (SIC) Production is projected to grow by 0.4%. Furthermore, Business Inventories are forecasted for a 0.2% rise, if they beat expectations and come in “hot” over the next couple prints, that should imply businesses are front running the risk of tariffs.

In housing, November’s Building Permits and Housing Starts are both expected to show increases, with Permits forecasted at 1430k from 1416k and Starts anticipated at 1345k from 1311k. The December NAHB Housing Market Index is anticipated for a slight rise to 47 from 46, and Existing Home Sales for November are projected to inch up to 4.10m from 3.96m.

On the macroeconomic front, next week brings a FOMC Rate Decision, with expectations of a 25-basis point cut, lowering the range to 4.5%-4.25% from 4.75%-4.5%. Q3 GDP has forecasts of remaining unchanged at 2.8%. Inflation data will include the highly watched by the Fed Personal Consumption Expenditure (PCE) report. PCE YoY is anticipated to rise to 2.5% from 2.3% and Core (Ex Food & Energy) PCE YoY is projected to tick up to 2.9% from 2.8%. The final December’s University of Michigan consumer surveys will be published. We are keeping an eye on the 5-10 Yr Inflation Expectations as a longer-term increase would signal heightened tariff risk on the part of the consumer.