Fundamental Report

Supply-Side Takeaway: Import arrivals surprised (slightly) to the upside, while domestic production continues to be somewhat restrained. Encouragingly, the global prices does appear to be stabilizing and moving up, now up for 2 consecutive weeks.

This week’s data: The Domestic – Global HRC price differential expanded as the domestic spot price rebound outpaced the further gain in the global average price. On the imports side, this week’s preliminary estimate for January arrivals indicate an increase from December’s census figure of just below 900k. Domestic production eased for a second consecutive week, stalling its recent upward trend.

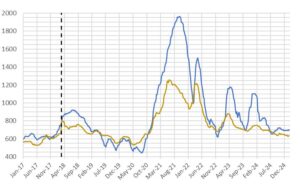

HRC Spot Prices – US Domestic & Global

- The global HRC spot price rose to $636 from$631. This week the price changes were from: +$21 in Europe, +$6 in Korea, +$2 in China, and -$3 in Turkey.

- The Domestic – Global HRC spread expanded, widening to $64.37 from $58.84.

Total Sheet Imports (s.ton)

- This week’s imports estimated sheet arrivals for January indicate an increase, rising to 904k tons from December’s census figure of 892k.

- The named countries from the filed trade petition represent nearly 80% of the expected total arrivals for coated products in 2024.

Domestic Production (s.ton)

- For the week ending on January 25th, capacity utilization ticked down by 0.1% to 73.7% and domestic raw steel production fell to 1.641m from 1.644m/tpw.

- This brings the year-to-date production to 5.878m, operating at a rate of 73.9%, +1.0% above this point last year.