Macro Flash Report

June Manufacturing Data

Takeaway: This month’s data show mixed readings, but mainly pointed to continued contraction within the sector. The divergence between the S&P Global & ISM Manufacturing PMIs around the 50 contraction/expansion threshold underscores the fact that the sector is facing strong headwinds and is currently not in a position to be a catalyst for a demand driven rally in steel pricing.

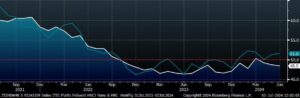

ISM Manufacturing PMI (white) & S&P Global Manufacturing PMI (blue)

The ISM Manufacturing PMI dropped unexpectedly to 48.5 from May’s 48.7, falling short of the 49.1 forecast. This marks the third consecutive month of declining activity and the lowest reading since February. The decline is mainly attributed to weak demand, reduced output, and accommodating input costs.

- Both production (48.5 vs. 50.2) and employment (49.3 vs. 51.1) saw contractions, while inventories (45.4 47.9) and backlog of orders (41.7 vs. 42.4) decreased at a faster pace.

- However, new orders (49.3 vs. 45.4) experienced a smaller contraction, and price pressures eased to their lowest since December (52.1 vs. 57).

- Additionally, the supplier deliveries index indicated faster deliveries (49.8 vs. 48.9).

The S&P Global US Manufacturing PMI was slightly revised down to 51.6 from a preliminary 51.7. Despite this minor revision, it marked its highest reading in three months, signaling improvement in the sector.

- New orders rose for the second consecutive month, and production continued to grow, though at a slower

- Employment saw its largest increase since September 2022. While input costs remained high, the rate of inflation eased, and selling prices increased at their slowest pace this year.

- However, business confidence dropped to a 19-month low, and client demand remained subdued.

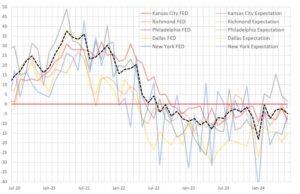

Accumulative Fed Surveys (black, dashed)

We can look to the June FED Manufacturing Surveys for some additional insight as to why the ISM PMI came in below expectations. While there were some positive signals for improvement early in the month, the full set of data came in slightly down.

- Empire (NY): -6.0 above -10 expected and up 9.6 MoM

- Philadelphia: 1.3 below 5 expected and down 3.2 MoM

- Dallas: -15.1 in line with expectations and up 4.3 MoM

- Kansas City: -8 below -5 expected and down 6 MoM

- Richmond: -10 below -3 expected and down 10 MoM

Looking forward, while some regions like NY Empire and Dallas showed signs of improvement and optimism for the future, others like Richmond and Kansas City continued to struggle. Overall, future outlooks and expectations indicate cautious optimism, despite ongoing challenges in certain areas.