Macro Flash Report

Industrial & Manufacturing Production

Takeaway:

Industrial production rebounded from July’s hurricane-related decline, exceeding market expectations and signaling a pickup in activity. However, the overall manufacturing landscape remains subdued, as high borrowing costs continue to restrain capital spending and dampen demand. With the Federal Reserve expected to begin cutting rates, this may boost investment and consumption, potentially stimulating demand for steel as the industrial sector looks to recover more robustly in the coming months.

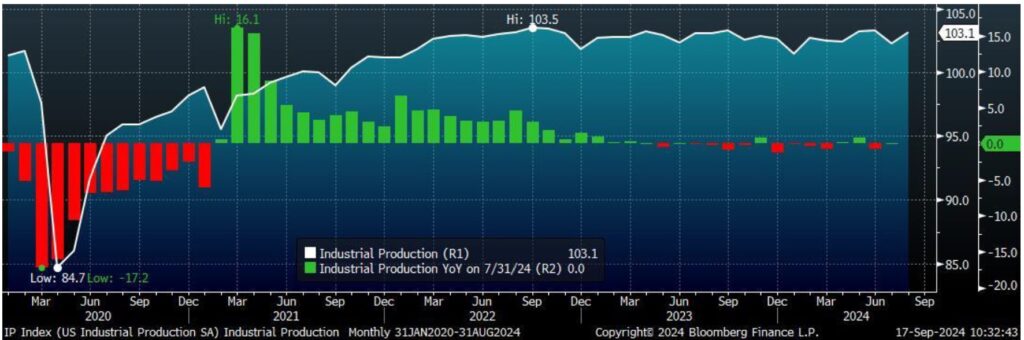

Industrial Production (YoY% Green/Red)

In August, Industrial Production rose by 0.8%, marking the largest monthly gain since February. This surpassed market expectations of a 0.2% increase and a rebound from last month’s hurricane-related low of -0.9%.

- Year-over-year, production was flat at 0% following a downwardly revised -0.7% decline in July.

Capacity Utilization improved to 78.0% in August, up from a downwardly revised 77.4% in July, although it fell short of the forecasted 79.9%. This rate is 1.7 percentage points below its long-run average.

Manufacturing (SIC) Production, which comprises 78% of total industrial output, advanced 0.9%, exceeding the anticipated 0.3% increase and recovering from a -0.7% decline in July.

- Annually, manufacturing production grew by 2%, after a downwardly revised -0.7% fall in July.

- Capacity utilization in manufacturing ticked up by 6% to 77.2%, still 1.1 percentage points under its long-term average.

- Durable goods manufacturing surged by 1%, up from a -1.5% decline in July, while nondurable manufacturing decreased by -0.2%.

- Notable movements included motor vehicles and parts (+9.8%), primary metals (+3.2%), and miscellaneous durable manufacturing (-0.9%).