Macro Flash Report

Initial & Continuing Jobless Claims

Takeaway:

Today’s improvement in initial jobless claims data clearly signals that the October payrolls number, (12k, versus the expected 100k) was an anomaly and the labor market remains healthy.

Initial & Continuing Jobless Claims

Initial Jobless Claims (dotted) declined to 213k on the period ending November 16t from the downwardly revised 219k and below market expectations of an increase to 220k. This marks the least number of individuals filling for unemployment benefits since April. Over the same period, Jobless Claims 4-week Average (solid) eased to 217.75k from the revised lower 221.50k. This is the fourth consecutive week of declines and the lowest reading since May.

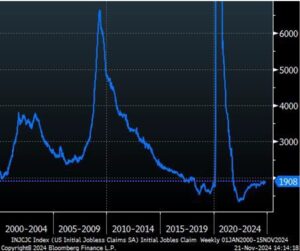

Continuing Jobless Claims (2000 – Current)

On the other hand, Continuing Jobless Claims (blue) climbed to 1,908k from the previous week’s upwardly revised 1,875k, surpassing the forecasted slight decline to 1,870k. Continuing Claims have been steadily rising, with this print reaching the highest level in three years. However, it’s important to point out that this upward trend is starting from historically unsustainable low levels (chart above).

Looking forward, October’s Nonfarm Payrolls saw the first decline since December 2020, falling to -28k. Reasons for this downturn have been attributed to the Boeing strike, as well as impacts from the hurricanes.

Notably, the response rate dropped to its lowest level since January 1991, which is also likely contributing to this sour reading. Considering this, along side the resolution of the Boeing strike and continued recovery from the hurricanes, has given us confidence that the figure released for November’s Nonfarm Payrolls will surpass market expectations.