Macro Flash Report

Fed Manufacturing Surveys

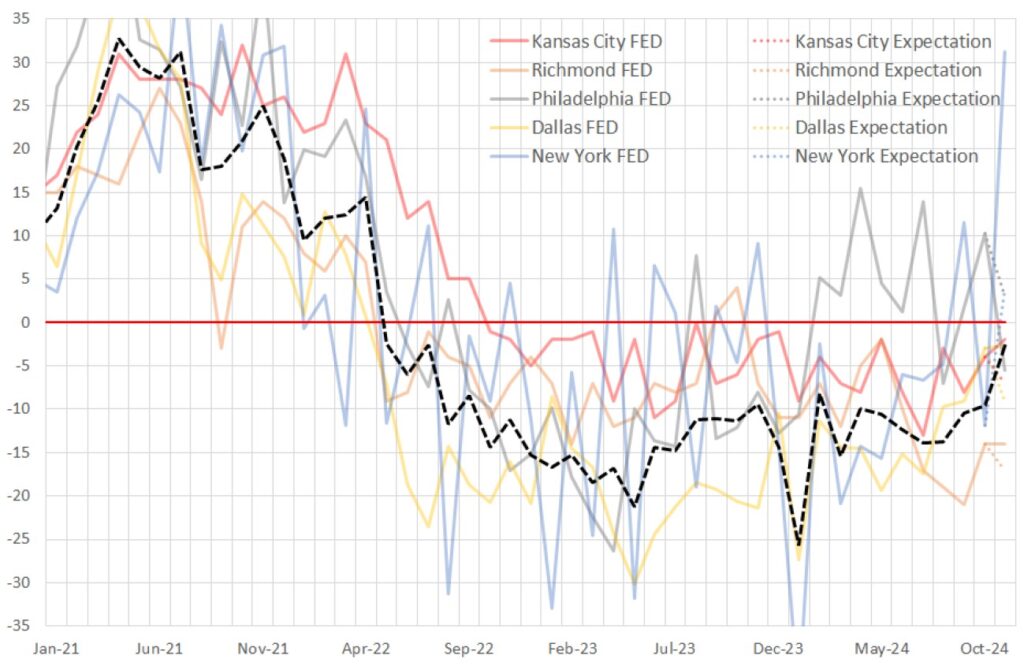

Takeaway:

The November FED Manufacturing Surveys in aggregate paint a picture of improvement within the sector that fails to push out of contraction territory. All that said, it continues to be encouraging that we have seen 4 consecutive months of improvement.

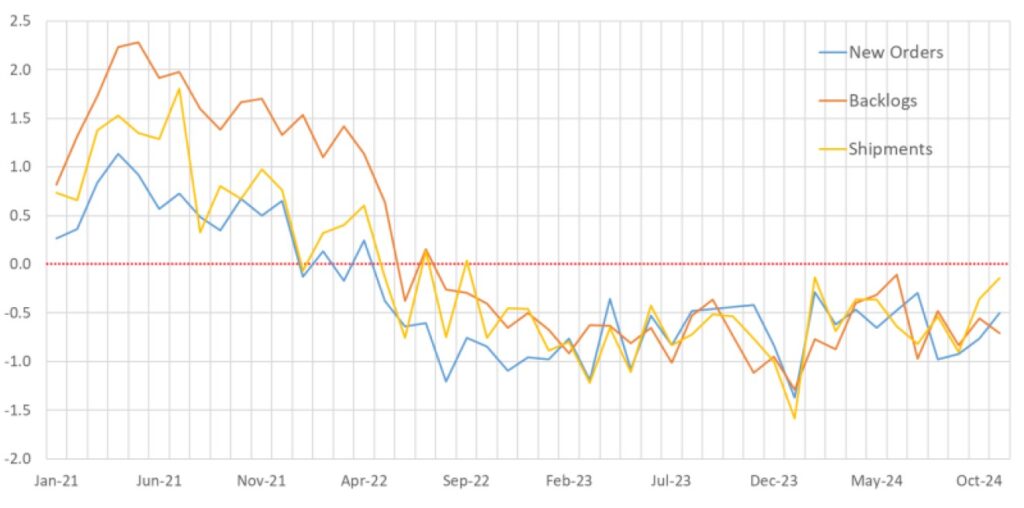

Aggregate Fed Manufacturing Surveys

NY Empire soared to 31.2, surpassing market expectations of 0 and up from -11.9 in October, marking the highest reading since December 2021.

- New orders (+38 to 28) and shipments (+35 to 32.5) experienced sharp increases.

- Six-month expectations remained firmly optimistic, albeit down slightly (33.2 vs 38.7).

Philadelphia declined to -5.5 from 10.3 in October, missing the forecasted 8. This marks the second contractionary reading since January.

- New orders (8.9 vs 14.2) and shipments (4.5 vs 7.4) fell but remained positive.

- Looking forward, six-month growth expectations reached the highest level since June 2021 (56.6 vs 36.7).

Kansas City improved to -2 from October’s -4, beating the anticipated dip to -5.

- Production (-4 vs 0) and new orders (-9 vs -5) both slipped.

- Expectations for future activity improved (11 vs 7).

Richmond held steady at -14, failing to reach the expected improvement to -10.

- Activity remained sluggish with shipments (-12 vs -8), new orders (-19 vs -17), and backlogs (-27 vs -14) worsening.

- Despite this, future expectations for local business conditions grew (31 vs 21).

Dallas rose to -2.7 from -3 in October, missing the forecasted improvement to -1.8. This represents the smallest contraction since negative reading began in May 2022.

- Production dropped sharply (-0.9 vs 14.6), and new orders declined further (-11.9 vs -3.7).

- Company outlook rose to expansion for the first time since early 2022 (5.8 vs -3.3), and six-month expectations held (31.2 vs 29.6).