Macro Flash Report

Inflation

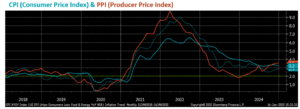

Takeaway:

This week’s December inflation data came in below expectations, temporarily pausing the sustained upward momentum that has developed over the last couple of months.

In December, Core (Ex Food & Energy) Consumer Price Index (CPI) YoY (solid) eased to 3.2%, below the expected 3.3% and down from 3.3% in the previous three months.

- The shelter index rose by 6%, marking the smallest annual gain since January 2022.

Core CPI MoM increased by 0.2% in December, easing from 0.3% in the last four months and lower than the anticipated 0.3%.

- Shelter remained unchanged at 0.3%, while transportation services rose sharply (0.5% vs 0%).

CPI YoY (dotted) rose by 2.9% in December, coming in line with the forecasts and up from November’s 2.7%. This marks the third consecutive month of increases, yet this rise was partly driven by low base effects from last year.

- Energy declined much less (-0.5% vs -3.2%). Food (2.5% vs 2.4%) and transportation (7.3% vs 7.1%) accelerated. Prices fell less for new vehicles (-0.4% vs -0.7%).

CPI MoM had a 0.4% increase, meeting the expected 0.4% and up from 0.3% in November. This marks the highest rate since March.

- Energy rose by 6%, accounting for over 40% of the monthly increase. Food prices went up by 0.3%.

Core (Ex Food & Energy) Producer Price Index (PPI) YoY (solid) increased by 3.5% in December, remaining unchanged from November and below the forecasted 3.8% rise.

Core PPI MoM was 0.0%, halting November’s 0.2% increase and below the anticipated 0.3%. This marks the first month where prices refrained from rising since July.

PPI YoY experienced a 3.3% increase, up from 3.0% in November and below the expected 3.5%. This marks the third consecutive month of increases and the highest rate since February 2023.

PPI MoM slowed to 0.2% from 0.4% in the prior month and short of the forecasted 0.4%.

- Prices for goods increased by 6%, driven by a 9.7% rise in gasoline. Prices for services held steady.