Macro Flash Report

Consumer Price Index (CPI)

Takeaway:

January’s CPI report exceeded market expectations, putting a pause on its once disinflationary trend. While this uptick in inflation can partly be attributed to seasonal and base effects, it has diminished the likelihood of more than one interest rate cut by the Federal Reserve this year.

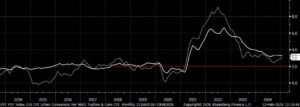

CPI YoY – Topline (Dotted) & Core (Solid)

In January, the Core (Ex Food & Energy) CPI YoY increased to 3.3% from 3.2% in the previous month, surpassing the market expected 3.1%.

- Prices accelerated for motor vehicle insurance (11.8% vs 11.3%) and transportation (8% vs 7.3%), while the shelter index slowed (4.4% vs 4.6%), the smallest 12-month gain since January 2022.

On a monthly basis, Core CPI rose by 0.4% from 0.2% in December, exceeding the anticipated 0.3%. This marks the sharpest rate increase since March 2024.

- Transportation services (1.8% vs 0.5%) and shelter (0.4% vs 0.3%) both rose at a faster pace, with shelter accounting for nearly 30% of the increase.

The topline CPI YoY similarly came in hot, advancing by 3% compared to the forecast of 2.9%, and up from December’s 2.9% increase.

- Energy costs marked their first increase in six months (1% vs -0.5%), while inflation for food steadied (2.5% vs 2.5%).

CPI MoM increased by 0.5% in January from 0.4% in the prior month, coming in above expectations of easing to 0.3%. This marks the highest rate since August 2023 and the third consecutive month of acceleration.

- Food prices increased (0.4% vs 3%) and energy costs slowed from December’s notable gain (1.1% vs 2.4%).