Macro Report

**Flash Report – 3Q23 GDP Final Revision**

Takeaway:

The final revision for 3Q23 GDP came in at 4.9%, slightly below estimates of 5.2%. In a year where expectations were for a recession, the overall economy has shown remarkable growth to date. This is the highest level of Seasonally Adjusted QoQ growth since 4Q21.

Key revisions:

Consumer spending on goods went to 4.9% from 4.7% while services spending reduced to 2.2% from 3%.

Gross private investment dipped to 10% from 10.5% (still red-hot remarkable growth).

Government consumption rose to 5.8% from 5.5%, driven

mostly by the increase in state and local spending.

The change in inventories were revised to $77.8B from

$83.9B. Up significantly from the 2Q23 change of $14.9B

Net Exports had very little impact and were essentially flat.

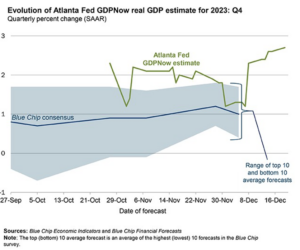

Looking forward, forecasts for 4Q23 have meaningfully improved since September. The Atlanta Fed GDPNow (Chart #2) forecast rose to an estimate of 2.7% growth (as of 12/14). Furthermore, the low end of the “Blue Chip” forecasters survey has been in growth territory since 11/6. Both of these tell a similar story of a rosier outlook, now that data for the 4th quarter is coming in.