Macro Report

Week’s Takeaway:

This week’s mixed results in the data did not provide a clear narrative, as the overall impact from the hurricanes work their way through the system. With election day next Tuesday, and the next FOMC decision on Wednesday, it will only take a few weeks for clarity on what the beginning of next years macro dynamics will be.

Notes:

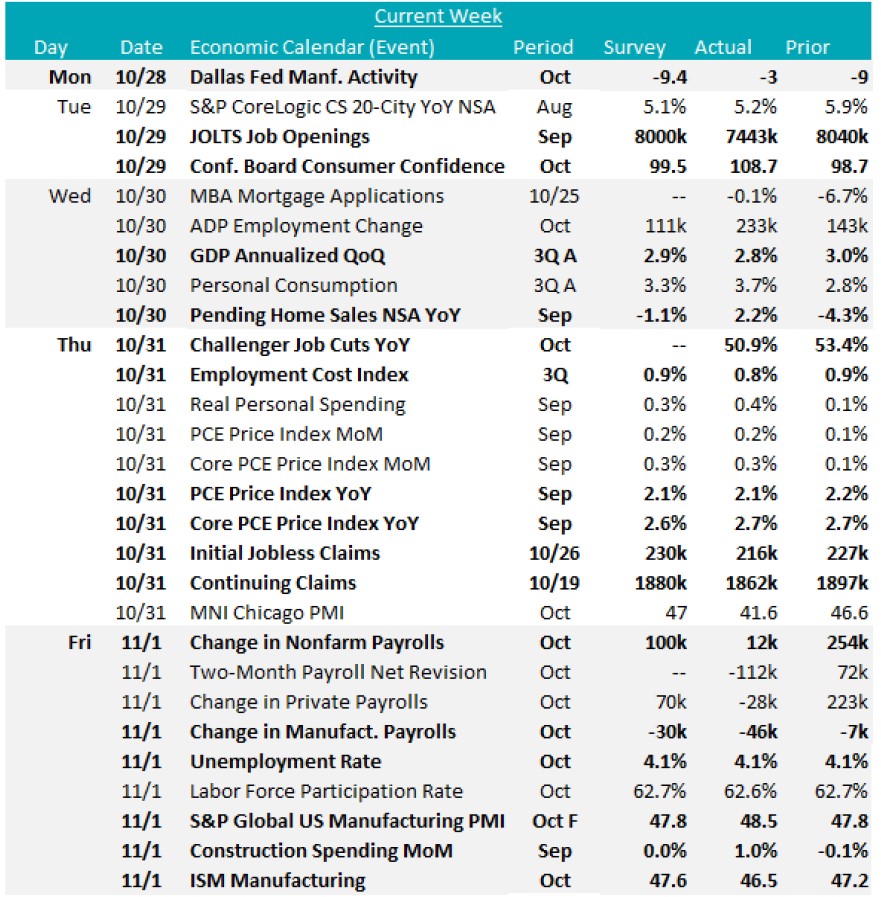

October manufacturing data highlights ongoing challenges in the sector while also showing some signs of improvement. The ISM Manufacturing PMI dropped to 46.5, missing the forecasted rise to 47.6 from September’s 47.2. Conversely, the final data for the S&P Global Manufacturing PMI rose to 48.5, exceeding the preliminary 47.8, yet still in contraction. Furthermore, most Fed Manufacturing Surveys surpassed market expectations – ex Empire (NY) – but the overall aggregate reading remains in contraction.

Construction Spending increased by 0.1% versus the anticipated 0.0%, with year-over-year growth up by 4.6% in September. Private spending was steady while public spending increased 0.5%.

September Topline PCE was down to 2.1% YoY, while Core PCE (the FED’s preferred inflation measure) remains elevated and increased on the month, up to 2.7% from 2.6% last month.

This week’s tranche of labor market data was incredibly varied. To start, Job openings decreased to 7.44M, moving below the pre-pandemic peak of 7.56M from November 2018. Job cuts were slightly lower, to 72,821 MoM and continue to bounce around the 60-90k range that we have been mostly stuck in since the end of 2022. The ECI (employment cost index) also came in slightly below expectations at 0.8% versus the expected 0.9% in 3Q24 (slightly elevated, but not inflationary). while initial and continuing claims both came in under expectations, a sign that the impact of the hurricane is almost fully removed once we clear the month of October. The former conclusion is important when viewing the significant downside surprise in the change non-farm payrolls which came in at 12k jobs added versus an expected 100k. What’s interesting, is that this reading stands in stark contrast to what we saw in the ADP employment data, which showed 233k jobs added, versus the expectation of 111k. Finally, the unemployment rate held at 4.1%.

Next Week’s Notes:

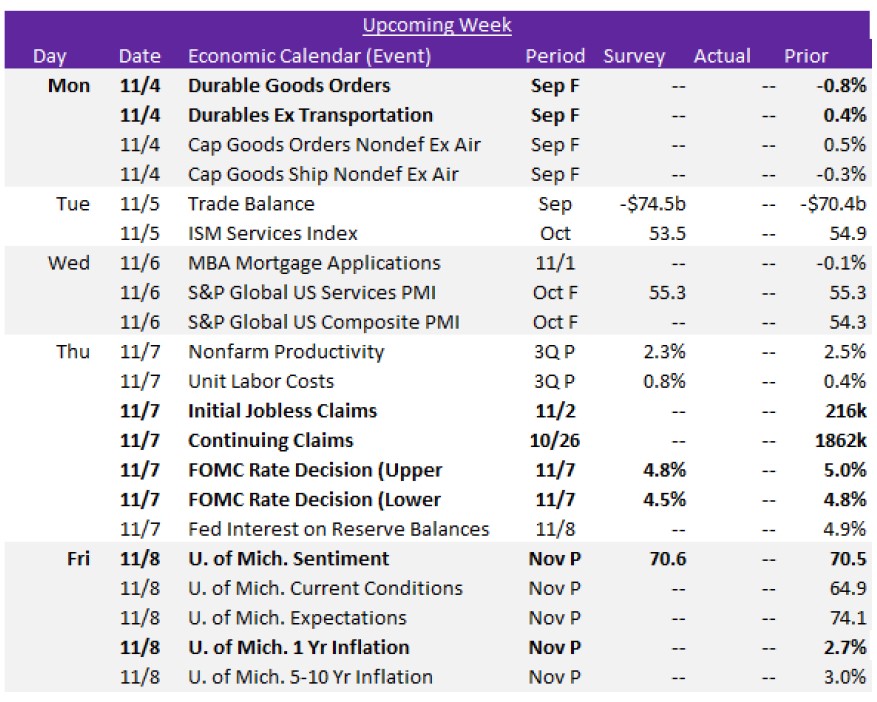

Next week will bring insights on manufacturing orders, alongside other economic indicators and a Federal Open Market Committee (FOMC) rate decision.

The final reading for September’s Durable Goods Orders are set to be released, with preliminary findings showing a second consecutive decline of -0.8%. In contrast, Durables Ex Transportation showed a 0.4% increase, marking the second month of growth. This signals that the transportation sector’s demand is weakened, dragging on orders.

In the upcoming week, we will also receive the weekly updates on Initial and Continuing Jobless Claims, as well as preliminary results from November’s University of Michigan consumer surveys. The Sentiment Index is forecasted to tick up slightly to 70.6 from 70.5, which would represent the fourth consecutive monthly increase and reach the highest level since April.

Finally, the FOMC will announce their Rate Decision. Market expectations are for a 25 basis point (bps) cut following the initial 50 bps reduction in September, which would lower interest rates to the 4.50% – 4.75% range from the current 4.75% – 5.00%. As of today, the CME FedWatch Tool indicated a 99.7% probability of this cut, with an 82.8% chance of an additional quarter-point reduction in December.