Macro Report

Week’s Takeaway:

This week’s data continues the recent theme of disappointing current activity with near term optimism on the industrial side. The broader economy on the other hand showed further signs of resilience as the FED signaled a slower pace of cuts next year.

Notes:

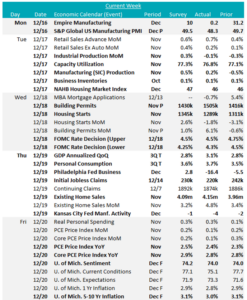

Manufacturing data failed to follow through on some of the earlier positive sentiment data this week, with all three Fed Manufacturing Surveys falling well below expectations: the NY Empire Index came in at 0.2 vs the expected 10, the Philadelphia Index dropped to -16.4 vs the anticipated 2.8, and the Kansas City Index fell to -4 vs the forecasted -1. Additionally, the preliminary December results for the S&P Global US Manufacturing PMI fell to 48.3, missing the anticipated slight dip to 49.5 from 49.7 in November.

Furthermore, Industrial Production also underperformed, declining by -0.1% in November, vs the forecasted 0.3% gain, with Capacity Utilization dipping to 76.8%, missing the expected increase to 77.3%. Manufacturing (SIC) Production increased by 0.2% but fell short of the 0.5% forecast.

In housing, the NAHB Housing Market Index remained steady at 46 in December, below the expected 47. Housing Starts also disappointed, dropping to 1289k, against the expected increase to 1345k from 1311k. However, Building Permits exceeded expectations, rising to 1505k from 1416k, surpassing the forecasted 1430k. Existing Home Sales rose to 4.15m in November, above the expected 4.09m.

The third and final revision for Q3 2024 GDP show that the economy grew at an annualized rate of 3.1%, up from 3.0% in Q2 and better than the second estimate of 2.8% – marking the highest growth rate so far this year. Finally, the FOMC voted to cut the Fed Funds rate by 25 bps to 4.5-4.25%, as the market expected. More notably, expectations for cuts next year were reduced from 4 cuts (100bps) to 2 (5 bps).

Next Week’s Notes:

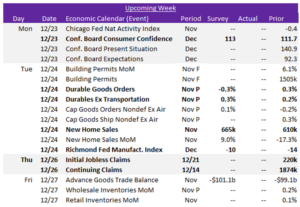

Next week will be light in terms of data releases.

We will receive another Fed Manufacturing Survey, the Richmond index, which has market expectations of improving to -10 from -14 in November. Additionally, the preliminary results for November’s Durable Goods Orders are forecasted to show a -0.3% decline from the 0.3% increase in October. However, Durables Ex Transportation is anticipated to rise by 0.3% from the 0.2% gain in the prior month.

More housing data for November will be released next week, with New Home Sales projected to increase to 665k from 610k.

Lastly, on the macroeconomic front, the Conference Board Consumer Confidence index for December is expected to climb to 113 from 111.7.