Fundamental Report

Supply-Side Takeaway:

Available supply is increasing as steel prices remain subdued. Recent price announcements have shifted the near-term narrative, but a price reversal will likely be short lived without a follow through in demand.

This week, the U.S. Domestic – Global price differential expanded slightly, due to the US price holding steady, while the global average decreased marginally. For imports, preliminary data for February arrivals continues to suggest a slight reduction in imports, likely reflecting the supply chain disruptions and shipping delays impact. However, a first glimpse at March’s arrivals has preliminary data showing a notable increase, clearly indicating a robust trend higher for imports. Meanwhile, US domestic production, after experiencing a slight pull back in the week prior, continued its upward trend, ramping up to its highest level since September 2023.

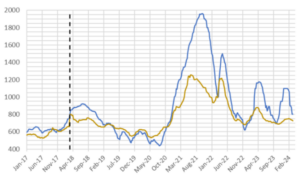

HRC Spot Prices – US Domestic (Blue) & Global (Gold)

- The global HRC spot price fell to $726.67 from $733.33, primarily due to a $23 decrease from Turkey, as well as a $10 decline from Korea, and -$7 from Europe.

- The Domestic – Global HRC spread slightly widened, rising by $6.66 to $73.33, remaining at the lowest level seen since October 2023.

Total Sheet Imports (s.ton)

- Imports estimated sheet arrivals for March point to a continued trend higher, rising to 944k from February’s estimated slight slump in arrivals of 829k. This week’s preliminary data for March, if realized, would reach the highest level of import arrivals since August 2022.

- Supply chain issues and shipping delays could be the reason for the mere reduction seen in February’s estimates. However, preliminary data is showing a trend higher in imports.

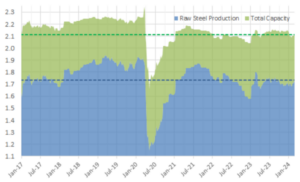

Domestic Production (s.ton)

- For the week ending on March 9th, capacity utilization ticked up by 0.8% to 78.1%, marking the highest rate since June 2023. At the same time, domestic raw steel production jumped up to 1.734m from 1.716m net tons. This is the nearest it has been to the historical average and post-pandemic average since September 2023.

- This brings the year-to-date production to 16.593m, operating at a rate of 75.8%. This marks a -3.3% decrease from the same timeframe in the previous year, when production was at 17.168m with a capacity utilization rate of 77.7%.