Fundamental Report

Supply-Side Takeaway:

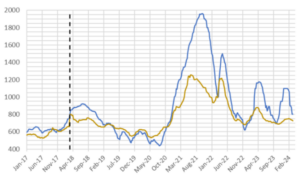

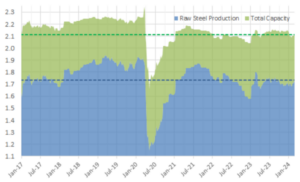

Import arrivals continue to climb and domestic production remains elevated. The U.S. and global HRC spot prices converged further as the domestic market works through a surplus of material.

The Domestic – Global HRC price differential contracted further, mainly due to the domestic spot price declining while the global average held steady. For imports, the preliminary data for May arrivals continue to indicate a trend higher, notably increasing from April’s preliminary estimate, pointing to a level just above 1.1M st./m. Meanwhile, domestic production ticked up for the second consecutive week, suggesting a potential upward trend forming after recent low reached two-weeks ago.

HRC Spot Prices – US Domestic & Global

- The global HRC spot price was flat at $697. This week main price movements were from China, which rose by $5, and from Russia, which declined by $6. The global average has been gradual inching back towards $700 for the past several weeks.

- The Domestic – Global HRC spread contracted for the second week in a row, narrowing by $15 to $108.

Total Sheet Imports (s.ton)

- Imports estimated sheet arrivals for May indicate a continued trend higher for imports, soaring to 1M tons from April’s preliminary figure of 973k, both pointing to levels not seen since 2022.

- Potentially seeing the impact/roll over from the shipping delays caused by the supply chain disruptions.

Domestic Production (s.ton)

- For the week ending on May 11h, capacity utilization ticked up by 0.2% to 77.2% and domestic raw steel production climbed to 1.715m from 1.709m/tpw.

- This brings the year-to-date production to 31.974m, operating at a rate of 3%, -2.8% below this point last year.