Fundamental Report

Supply-Side Takeaway:

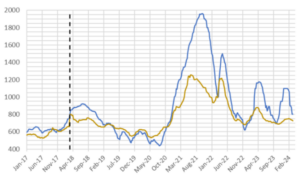

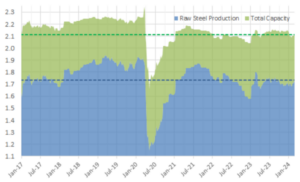

Import arrivals trend higher, while domestic production is at the higher level of its recent range. Domestic spot prices search for a bottom as we continue converging with the global price.

Domestic – Global HRC price differential contracted significantly, mainly due to the domestic spot price dropping while the global average edged slightly lower, hitting the lowest level since pre-mini rally in early March. For imports, the preliminary data for May arrivals continue to indicate a trend higher, pointing to a level just above 1M st./m and notably increasing from April’s final census data, which reached a level not seen since August 2022. Meanwhile, domestic production increased for the third consecutive week, reaching the highest level since early April.

HRC Spot Prices – US Domestic & Global

- The global HRC spot price was fell by $2 to $695. This week main price movements were from Turkey, which dropped by $11, and from Europe, which rose by $6. Additionally, China and Korea both declined by $3.

- The Domestic – Global HRC spread contracted significantly this week, narrowing by $43 to $65, reaching a level not seen since pre-mini rally, the beginning of March.

Total Sheet Imports (s.ton)

- This week’s imports estimated sheet arrivals for May continue to indicate a trend higher for imports, soaring to 1.048M tons from April’s final census data figure of 987k, both pointing to levels not seen since 2022.

- Potentially seeing the impact/roll over from the shipping delays caused by the supply chain disruptions.

Domestic Production (s.ton)

- For the week ending on May 18th, capacity utilization ticked up by 0.6% to 77.8% and domestic raw steel production climbed to 1.728m from 1.715m/tpw.

- This brings the year-to-date production to 33.702m, operating at a rate of 4%, -2.8% below this point last year.