Fundamental Report

Supply-Side Takeaway: The Initial look at June imports surprisingly suggests that arrivals have yet to substantially subside from elevated levels, while domestic production dropped after 5 weeks of incremental growth. Although the step lower in domestic production is a positive development, the overall current market surplus continues to be a significant obstacle for higher domestic pricing.

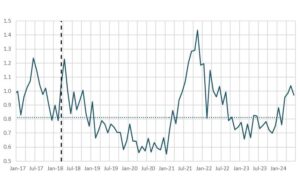

The Domestic – Global HRC price differential contracted, mainly due to the domestic spot price declining further while the global average stayed stagnant. For imports, the preliminary data for June arrivals indicate an easing, albeit still elevated level, of imports from May’s estimate, which is pointing to a level just above 1M st./m. Meanwhile, domestic production retreated sharply after five consecutive weeks of increasing.

HRC Spot Prices – US Domestic (blue) & Global (gold)

- The global HRC spot price held steady at $695. This week main price movements were from Europe, which rose by $8, China declined by $1, and Korea fell by $5.

- The Domestic – Global HRC spread contracted this week, narrowing from $55 to $45, its lowest level since October

Total Sheet Imports (s.ton)

- This week’s imports estimated sheet arrivals for June indicate a slight easing for imports, declining to 973k tons from May’s estimate figure of 1038k.

- Potentially seeing the impact/roll over from the shipping delays caused by the supply chain disruptions.

Domestic Production (s.ton)

- For the week ending on June 8th, capacity utilization ticked down by 2% to 77.3% and domestic raw steel production declined to 1.716m from 1.743m/tpw.

- This brings the year-to-date production to 38.790m, operating at a rate of 4%, -2.8% below this point last year.