Macro Report

Takeaway:

This week’s data signal that inflation is cooling, and consumer/labor market is holding up, while industrials remain sluggish. Altogether, there is more than enough evidence that the FED can begin the cutting cycle, but even then, it will take time for manufacturing activity to reach its potential.

Notes:

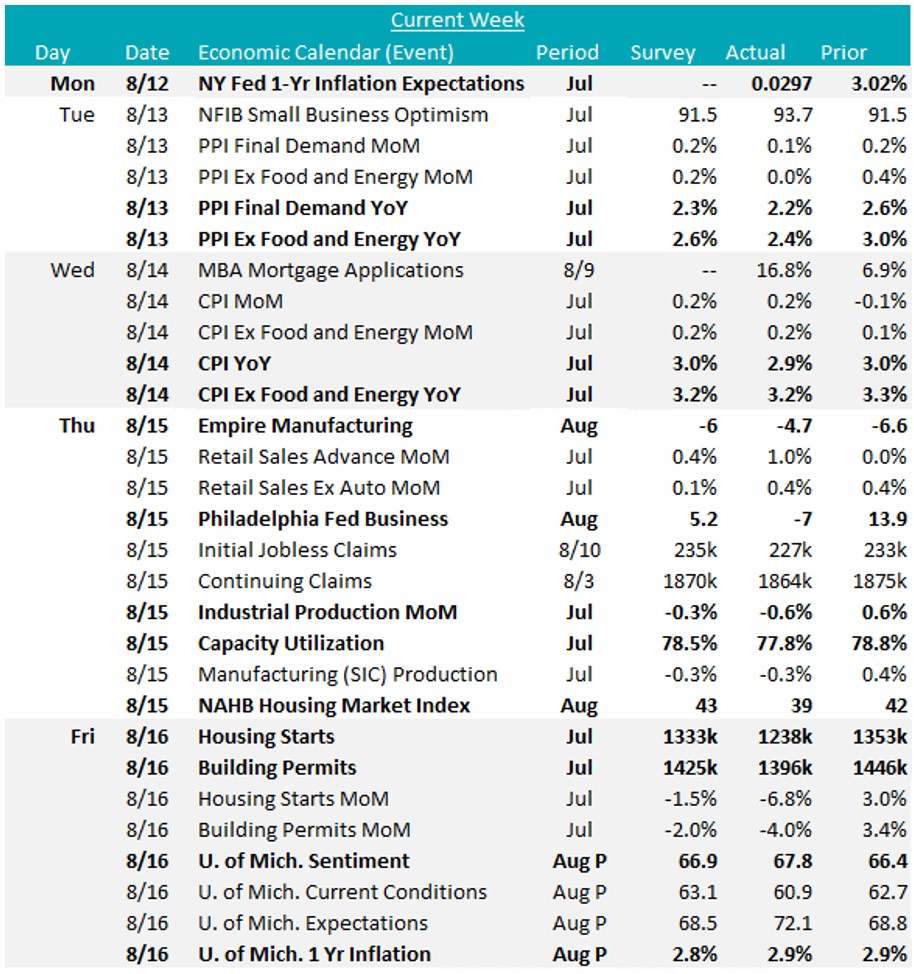

This week’s highlight was the cooling inflation data, reinforcing expectations for a September rate cut. The Core (Ex Food & Energy) Consumer Price Index (CPI) YoY rose 3.2% in July, marking the lowest pace in over 3 years. The headline CPI YoY increased by 2.9% vs the forecasted 3.0%. The Core Producer Price Index (PPI) YoY rose 2.4% in July vs the anticipated 2.7%, while the overall PPI YoY was also below expectations, 2.2% vs 2.3%. This easing was largely due to a decline services, signaling a broader moderation in inflation pressures. Regarding inflation outlook, the NY Fed 1-Yr Inflation Expectations held steady at 3.0%, and similarly, the University of Michigan’s preliminary August results for 1-Yr Inflation Expectations remained at 2.9%, a tick above the forecasted 2.8%.

The first 2 of the 5 FED Manufacturing Surveys for August were released and highlighted the sectors ongoing challenges as it continues to struggle with the pressures of high interest rates. The Philadelphia index, which had been the strongest among the regional surveys, unexpectedly dropped to -7 vs the forecasted 5.2, the first contraction since January. Conversely, the NY Empire index exceeded expectations, rising to -4.7 vs -6, the highest reading in six months, albeit still in contraction. Additionally, July’s Industrial Production also showed signs of weakness, falling by -0.6% vs a -0.3% decline, with Capacity Utilization ticking down to 77.8% vs the forecasted dip to 78.5%.

However, this larger-than-anticipated drop has been mainly attributed to the disruptive impact of Hurricane Beryl. These results suggest a cautious outlook moving forward.

Finally, the first round of housing data for July came through with Housing Starts and Building Permits both coming in down and worse than expected, (-6.8%, vs exp. -1.5%), and (-4%, vs exp. -2%), respectively. Furthermore, the NAHB Housing Market Index fell to 39, from 42 in August. Taking a step back, it is important to remember that the recent step lower in interest rates only occurred in the last two weeks.

Next Week’s Notes:

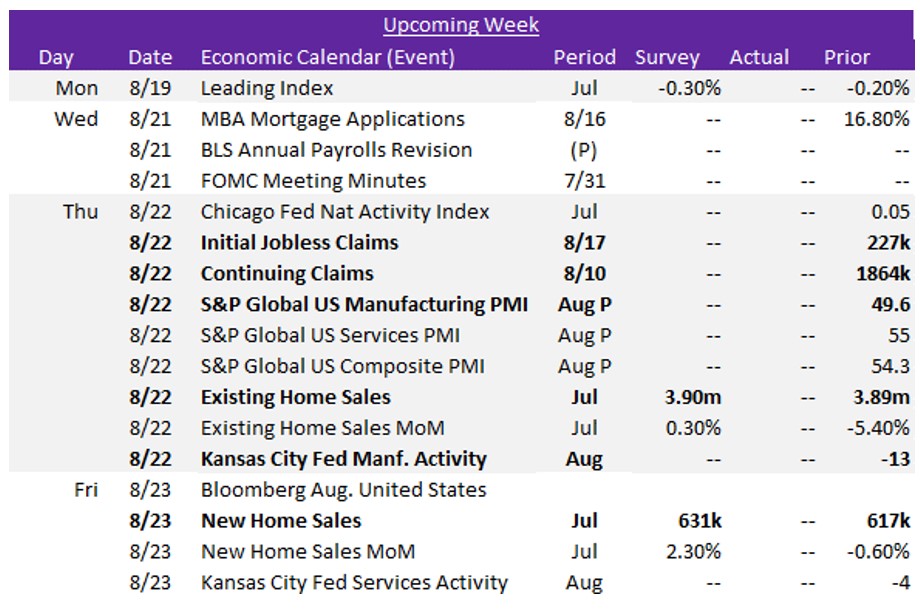

Next week, key steel-specific sector data and labor market updates will be released that will help shape expectations for both the steel sector and the broader economy.

For the manufacturing sector, we’ll receive the preliminary results for the August S&P Global US Manufacturing PMI, along with another FED Manufacturing Survey, the Kansas City index, for the same month. These reports will provide early indications of current manufacturing activity.

The housing market will also be in focus, with July’s Existing Home Sales forecasted to edge up to 3.90m from 3.89m in June. New Home Sales are anticipated to rise to 631k in July from 617k. These projected figures suggest expectations for an uptick in housing demand.

Lastly, the weekly update on Initial and Continuing Jobless Claims will be reported and closely watched as they will provide further signals on the health of the labor market after showing some stability.