Fundamental Report

Supply-Side Takeaway:

Imports and Domestic production continue to slowly decline as we start maintenance outage season. The global price fell further while domestic pricing continues to bubble up.

This week’s data:

The Domestic – Global HRC price differential expanded further as the domestic spot price remained stable while the global average price declined. On the imports side, we receive our first glimpse at September arrivals, which preliminary estimate indicated a continued easing from August’s import estimate. Domestic production ticked down, dropping to its lowest level since early August yet maintains above the long-term average.

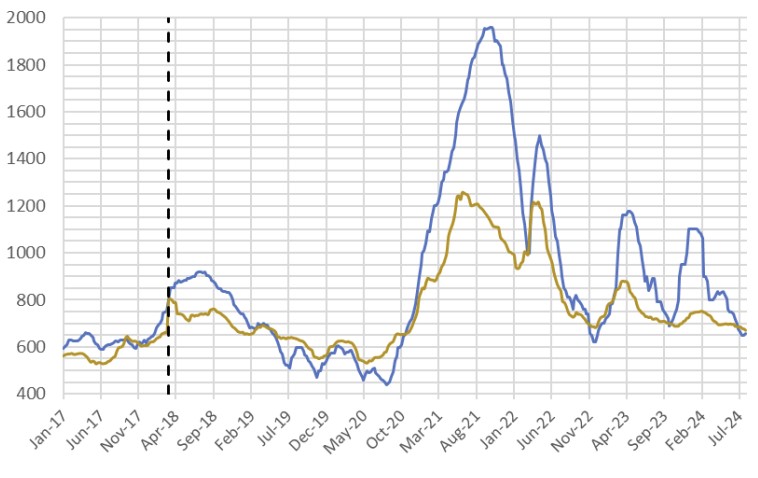

HRC Spot Prices – US Domestic & Global

HRC Spot Prices – US Domestic & Global

- The global HRC spot price fell to $637 from $642. This week the price changes were from: -$17 in Europe, +$14 in China and Korea, -$31 in Russia, -$8 in Turkey, and -$5 in Brazil.

- The Domestic – Global HRC spread expanded further, widening from $57.60 to $63.28, the highest differential since May.

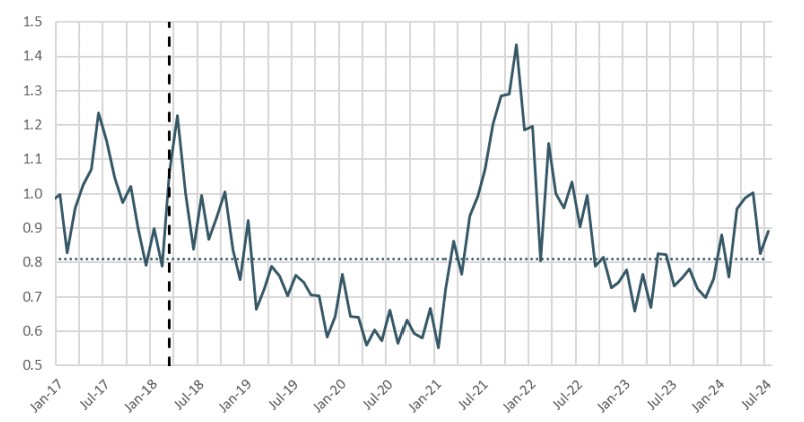

Total Sheet Imports (s.ton)

- This week’s imports estimated sheet arrivals for September indicate a continued decline, falling to 856k tons from August’s preliminary data estimate figure of 909k.

- It is highly unlikely that we would see another surge in arrivals for the remainder of the year. That said, we do anticipate some volatility in these figures as we push below the longer run “neutral level”.

- The named countries from the filed trade petition represent nearly 80% of the expected total arrivals for coated products in 2024.

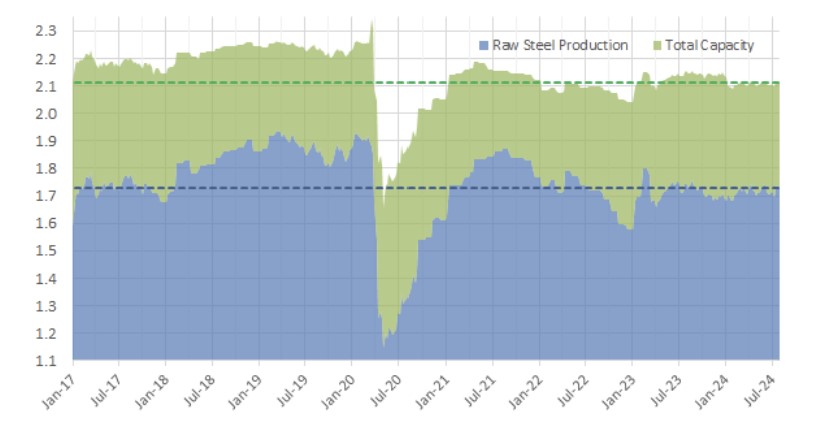

Domestic Production (s.ton)

- For the week ending on September 14th, capacity utilization ticked down by 1.0% to 78.8% and domestic raw steel production fell to 1.749m from 1.772m/tpw.

- This brings the year-to-date production to 62.859m, operating at a rate of 76.8%, -1.7% below this point last year.