Fundamental Report

Supply-Side Takeaway:

Domestic production is decreasing more significantly than in a typical outage season, while import arrivals continue slowly trending lower. Global prices were mixed but mostly higher while the domestic price was unchanged.

This week’s data: The Domestic – Global HRC price differential tightened further this week as the domestic price held steady while Chinese, ASEAN, and Turkish prices drove the global average higher. On the imports side, this week’s estimate for September arrivals indicated a further reduction in arrivals, now just below 900k. Domestic production fell sharply, now down to its lowest level since December 2022.

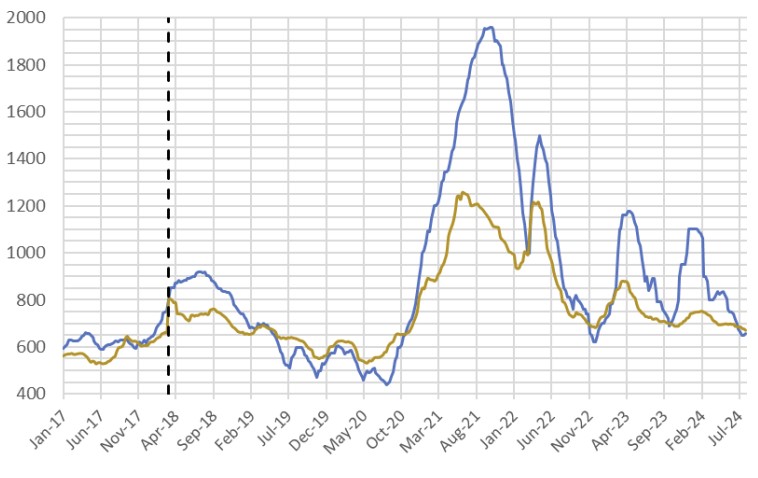

HRC Spot Prices – US Domestic & Global

HRC Spot Prices – US Domestic & Global

- The global HRC spot price rose to $655 from $646. This week the price changes were from: +$28 in Turkey, +$23 in China, +$9 in Korea, and -$5 in Europe.

- The Domestic – Global HRC spread contracted for the second consecutive week, narrowing to $65.38 from $74.50.

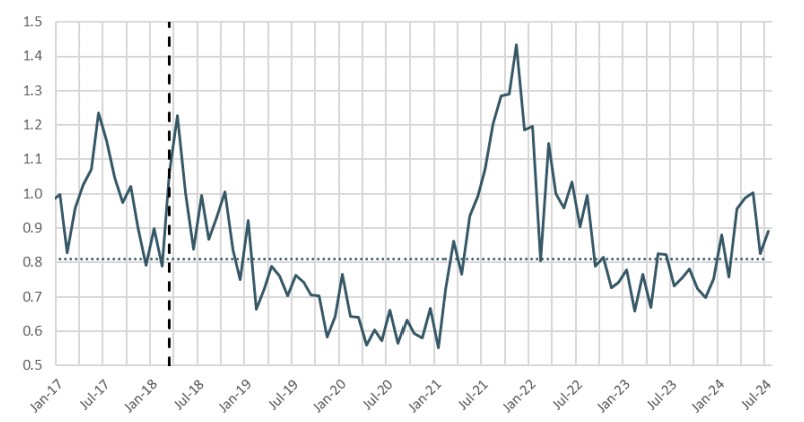

Total Sheet Imports (s.ton)

Total Sheet Imports (s.ton)

- This week’s imports estimated sheet arrivals for September indicate a continued decline, falling to 894k tons from August’s final census data figure of 918k.

- The named countries from the filed trade petition represent nearly 80% of the expected total arrivals for coated products in 2024.

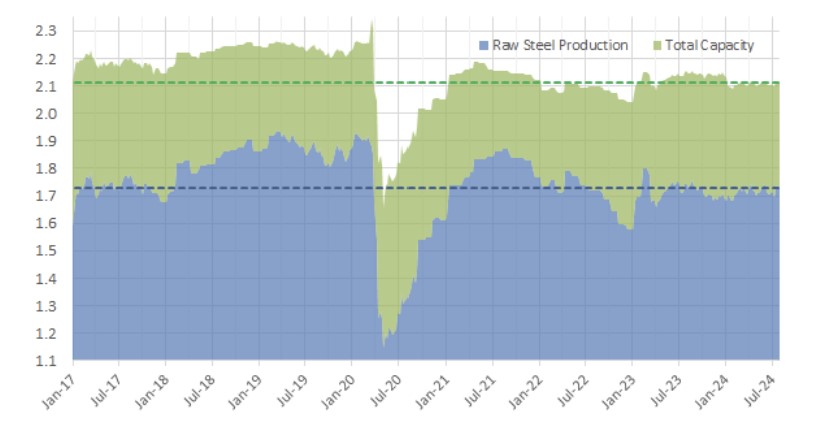

Domestic Production (s.ton)

Domestic Production (s.ton)

- For the week ending on October 5th, capacity utilization jumped down by 1.8% to 72.3% and domestic raw steel production fell to 1.606m from 1.646m/tpw.

- This brings the year-to-date production to 67.818m, operating at a rate of 76.6%, -1.7% below this point last year.