Fundamental Report

Supply-Side Takeaway:

The November import arrivals estimate remains elevated, while domestic mills are keeping production restrained going into the end of the year as they attempt to reduce the existing surplus. Spot HRC pricing remains under pressure, globally.

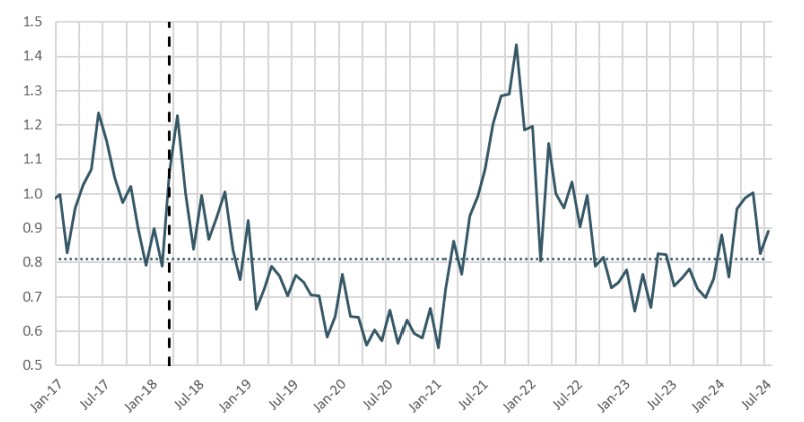

This week’s data: The Domestic – Global HRC price differential tightened further this week as the domestic spot price held steady while the global average price increased. On the imports side, this week’s estimate for October arrivals continues to indicate an increase, while November’s imports show easing to below the 900k level. Domestic production ticked back down, remaining subdued.

HRC Spot Prices – US Domestic & Global

- The global HRC spot price rose to $653 from $649. This week the price changes were from: +$23 in Brazil, +$17 in Russia, -$10 in China, -$5 in Korea, and -$4 in Europe.

- This marks the fifth consecutive week of the global price being bound by the range of $653 – $649.

- The Domestic – Global HRC spread contracted further, narrowing to $47.47 from $50.89.

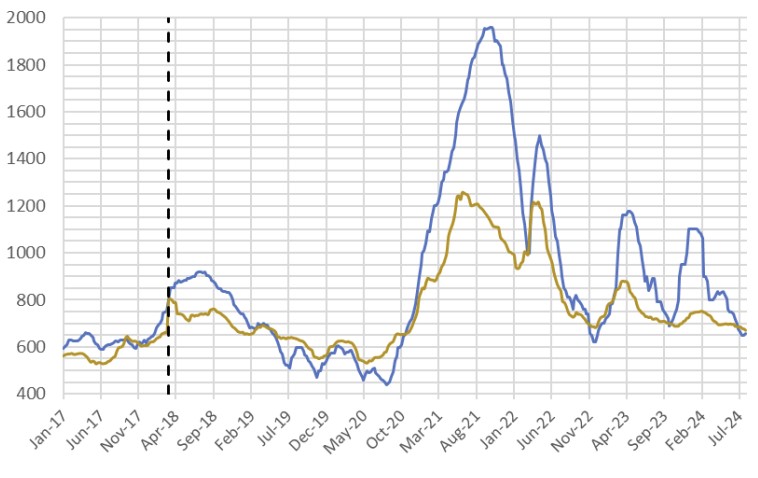

Total Sheet Imports (s.ton)

- This week’s imports estimated sheet arrivals for November indicate further easing, declining to 879k tons from October’s estimate figure of 910k.

- The named countries from the filed trade petition represent nearly 80% of the expected total arrivals for coated products in 2024.

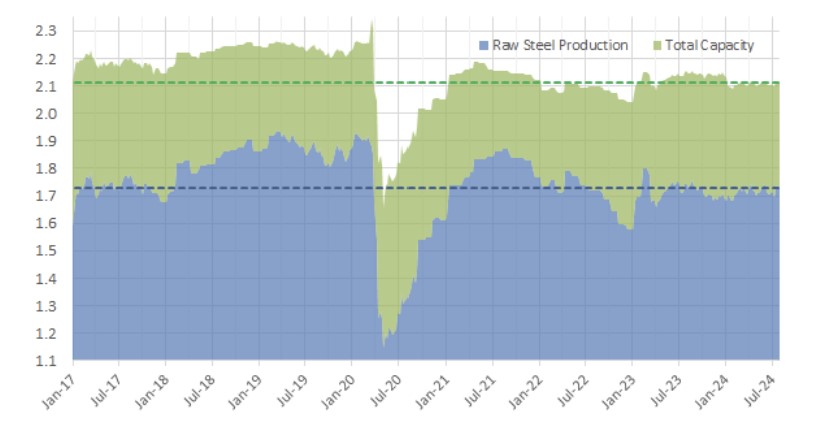

Domestic Production (s.ton)

- For the week ending on November 16th, capacity utilization ticked down by 1.1% to 73.1% and domestic raw steel production fell to 1.623m from 1.649m/tpw.

- This brings the year-to-date production to 77.383m, operating at a rate of 760%, -2.1% below this point last year.