Fundamental Report

Supply-Side Takeaway: Supply remains somewhat restrained with imports in their continued downtrend and domestic production below it’s long-run average. Global prices remain under significant pressure, which led to an expansion of the Domestic-global differential.

This week’s data: The Domestic – Global HRC price differential expanded as the domestic spot price increased while the global average price slipped further. On the imports side, we received a first look at January arrivals, which indicate a slight easing from December’s preliminary estimate, which continue to indicate a sharp rebound. Domestic production ticked back up after declining for two consecutive weeks.

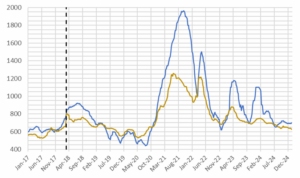

HRC Spot Prices – US Domestic & Global

- The global HRC spot price declined to $627 from $637. This week the price changes were from: -$28 in Russia, -$16 in China, -$13 in Korea, -$11 in Turkey, and +$6 in Europe.

- The Domestic – Global HRC spread expanded further, widening to $73.50 from $53.12, the highest since September.

Total Sheet Imports (s.ton)

Total Sheet Imports (s.ton)

- This week’s imports estimated sheet arrivals for January indicate a slight easing, falling to 857k tons from December’s preliminary figure of 887k.

- The named countries from the filed trade petition represent nearly 80% of the expected total arrivals for coated products in 2024.

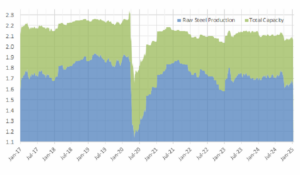

Domestic Production (s.ton)

Domestic Production (s.ton)

- For the week ending on January 11th, capacity utilization ticked up by 0.9% to 74.5% and domestic raw steel production rose to 1.659m from 1.635m/tpw.

- This brings the year-to-date production to 2.593m, operating at a rate of 1%, +1.3% above this point last year.