Fundamental Report

Supply-Side Takeaway:

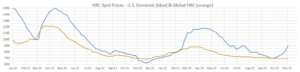

Prices around the world are rising fast, led by U.S. domestic prices. The primary risk to this rally in the near-term would be that the expected global production cuts do not materialize.

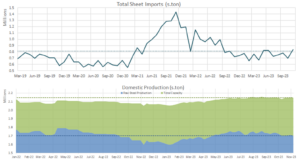

The Domestic – Global differential expanded further, US prices continue to outpace also rising global prices. Early imports show signs of an increase amid supply restraints. Finally, capacity utilization ticked down, after two weeks of increases.

Notes:

- The global HRC price had its largest percentage increase since converging with the US domestic HRC price. This was mainly driven by Europe, who saw a 7.1% increase. However, due to the domestic’s rate of increases in price, the US domestic HRC – global HRC spread increased to $203. This is the highest the spread has been since early June, but with Europe and China trending higher, higher domestic prices will be supported.

- November import data suggests that sheet arrivals will grow to 833k, up 5% from October, this would be the highest level seen since August 2022. Our October estimate for arrivals pushed a bit higher, with most recent data suggesting ~697k of arrivals.

- Capacity utilization ticked down by 4% to a rate of 73.9%, bringing domestic raw steel production down to 1.69M net tons.