Macro Flash Report

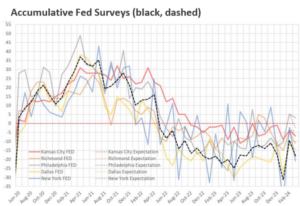

FED MANUFACTURING SURVEYS

March’s Fed manufacturing surveys disappointed compared to market expectations and showed overall declines across the board. There were signals of a burgeoning recovery in the first two months of the year, however, recent data shows that there are still significant headwinds in the manufacturing sector.

The “Accumulative Fed Survey” index tracks well with the closely watched ISM Manufacturing PMI, which will be released on Monday April 1st and is currently expected to increase slightly, from 47.8 to 48.5. If the index remains below 50 (the expansion/contraction threshold) it will be the 17th straight month of contraction in the sector, the longest streak since 2002.

NY Empire plummeted to -20.9, a steep decline from February’s

-2.4 and significantly below the forecasted -7.

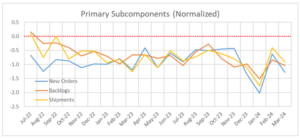

- This drop was characterized by a sharp decrease in new orders (-6.3 to -17.2) and shipments (2.8 to -6.9), alongside weakened labor market indicators.

- Despite this, six-month expectations are for improvements (21.5 to 21.6), although tempered.

Dallas declined to -14.4 from -11.3, slipping below the market expected improvement of -10.

- This fall was marked by significant drops in new orders (5.2 to -11.8), the growth rate of orders (-5.5 to -19.8), shipments (0.1 to -15.4), and the company outlook index (-8.5 to -16.2), with labor market measures suggesting a slowdown.

- However, the six-month expectation, while weaker, remained positive (6.2 to 3), maintaining expansion for the first time since April 2022.

Philadelphia slightly decreased to 3.2 from February’s 5.2 but exceeded expectations of a fall to -2.5, marking the second consecutive month of expansionary readings.

- There was a positive turn in new orders (-5.2 to 5.4), with improvements in shipments (10.7 to 4) and unfilled orders (-11.7 to 1).

- The six-month expectation notably brightened (7.2 to 6), indicating a stronger consensus for growth overall.

Richmond dropped to -11 from the previous month’s -5, missing the forecast to stay stagnant at -5.

- While shipments marginally improved (-15 to -14), backlogs plunged (-15 to -25) and volume of new orders slumped (-5 to -17).

- The six-month outlook suggests continued optimism, though it has slightly dimmed, with projections for shipments and new orders easing to 19 from 22.

Kansas City fell to -7 from -4, continuing a seven-month contraction trend.

- Notable downturns were production (3 to -9), shipments (6 to -5), new orders (-2 to -17), and backlogs (-13 to -27).

- Six-month expectations slowed (2 to 1), although continued to remain in expansion.