Macro Flash Report

May’s Manufacturing PMIs

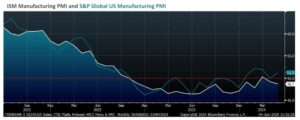

Takeaway:

May’s US Manufacturing PMIs provide a mixed view, with ISM slipping deeper into contraction, while S&P Global beat expectations with its 5th straight expansionary print. Given the broader context of recent soft industrial data, we hold the view that the market has already seen the worst of the downside, however, without an unexpected catalyst it will likely be a slow summer before a strong expansionary period begins.

The ISM Manufacturing PMI declined to 48.7 from 49.2 in April, falling short of the market expected rise to 49.6. This is the second consecutive month, as well as the 18th time in the last 19 months, of a contractionary reading. Key points include:

- New orders declined to 4 from 49.1.

- Inventories decreased to 9 from 48.2.

- Backlog of orders fell to 4 from 45.4.

- Production slowed to 2 from 51.3.

However, there were some positive developments:

- Employment rebounded to 1 from 48.6.

- Prices increased more slowly, rising to 57 from 9, as commodity driven costs climbed at a weaker rate – but remain in strong expansion.

- Supplier deliveries remained stable at 9

Overall, the report showed ongoing challenges with weak demand, as well as output being stable and inputs staying accommodative.

The S&P Global US Manufacturing PMI rose to 51.3, up from the preliminary 50.9 and from April’s 50. This marks the fifth straight expansionary reading, indicating a modest improvement in the sector’s health. Key insights include:

- New orders grew, driving faster production expansion, though the overall increase in new business was less than that of new export orders.

- Business confidence increase, leading to more hiring, higher purchasing activity, and a build-up of finished goods

On the pricing front:

- Input cost inflation accelerated to its highest rate in over a year, a 13-month high.

- Firms responded by raising their selling

Overall, the report showed signs of recovery, with improving demand and business confidence, despite rising input costs.