Macro Flash Report

Inflation

Takeaway:

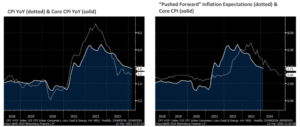

February’s CPI data came in slightly higher than market estimates, while forward-looking consumer inflation expectations held steady. While this was not a seismic increase, it is further evidence that January’s significant CPI upside surprise was not an anomaly. The fight against rising prices is not over and FED will need more evidence of disinflation before starting to cut interest rates.

CPI YoY rose slightly to 3.2%, up from 3.1% last month, surpassing the market expectations of holding steady at 3.1%. At the same time, the CPI (Ex Food & Energy) YoY fell to 3.8% from 3.9% the month prior and exceeding expectations of a drop to 3.7%.

One underlying trend which will require close attention in the coming months is Core Goods CPI, which showed a MoM increase (0.1%) for the first time in 8 consecutive months. Goods disinflation over much of last year was one of the primary drivers of the surprisingly fast deceleration in prices. We anticipate a steady recovery on the industrial activity side as we move into the 2nd half, potentially resulting in higher priced goods. If services and shelter prices do not start to push higher, this could be a significant risk for interest rate cuts this year.

*The market is currently pricing in the first cut in June, followed by 2 more by the end of the year.

The NY Fed 1-Yr Inflation Expectations remained unchanged at 3.0%, the same as in the previous two months, maintaining the three-year lows.