Macro Flash Report

FED MANUFACTURING SURVEYS

Takeaway:

The August FED Manufacturing Surveys paint a picture of suppressed activity overall in the month. While some regions improved, all of them are in contraction territory for the first time since February. On the steel consumption side, these sustained conditions highlight the ongoing dynamic that have pushed inventories to 2-year highs.

Aggregate FED Manufacturing Surveys

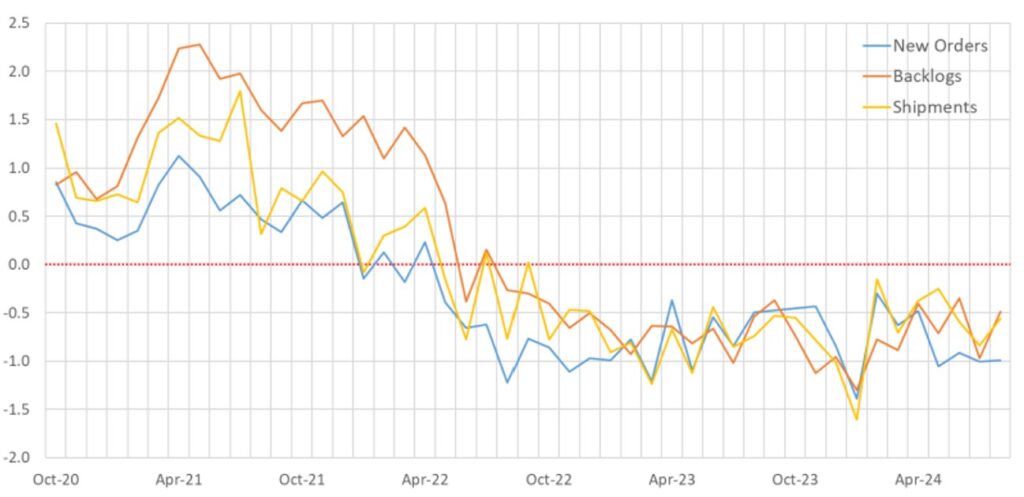

Primary Subcomponents

NY Empire rose to -4.7, a six-month high, improving from -6.6 in July and surpassing expectations of -6.

- New orders fell (-7.9 vs -0.6), but shipments remained steady (0.3 vs 3.9). Inventories declined for the second straight month (-10.6 vs -6.1).

- Employment dipped slightly (-6.7 vs -7.9), and hours worked dropping notably (-17.8 vs -0.1). Input costs rose more slowly (23.4 vs 26.5), while selling price increased modestly (8.5 vs 1).

- Despite challenges, firms remained cautiously optimism (22.9 vs 25.8).

Philadelphia dropped sharply to -7 from July’s 13.9, well below the anticipated 7, marking the first contraction since January.

- Shipments slowed (8.5 vs 8), new orders decreased (14.6 vs 20.7), backlogs shrank (3.2 vs 9.1).

- Employment turned negative (-5.7 vs 15.2) and price pressures persisted, with input costs rising (24 vs 19.8), though the pace of selling price increases slowed (13.7 vs 2).

- Future activity indicators weakened (15.4 vs 7).

Kansas City climbed to -3, up from -13 in July and outperforming the forecasted -9.

- Production hit a one-year high (6 vs -12). However, new orders (-12 vs -21) and backlogs (-19 vs -24) remained

- Employment continued to decline (-7 vs -12), as did hours worked (-10 vs -17).

- The future composite index rose (8 vs 5).

Dallas improved to -9.7 from -17.5 in July, marking the smallest contraction since January 2023.

- Production rebounded slightly (1.6 vs -1.3), and new orders rose (-4.2 vs -12.8). Shipments nearly reached positive territory (0.8 vs -16.3).

- Employment fell to near zero (-0.7 vs 1), indicating stability. Input costs increased sharply (28.2 vs 23.1), leading to higher selling prices (8.5 vs 3.4).

Richmond fell to -19 from -17 in July, marking the sharpest decline since May 2020 and the tenth month in contraction.

- New orders (-26 vs -23) and backlogs (-27 vs -20) worsened, while shipments rose slightly (-15 vs -21).

- Labor market conditions weakened, with employment dropping (-15 vs -5).

- Six-month expectation deteriorated, with local business conditions plunging (-18 vs 7).