Macro Flash Report

Manufacturing PMIs

Takeaway:

The November Manufacturing PMIs both came in above expectations, but as expected from Fed Manufacturing Surveys, they failed to push into expansion territory. The underlying data signals a continued recovery, with the new orders subcomponent reaching their highest respective levels in months.

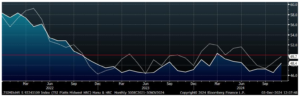

S&P Global US (dotted) & ISM Manufacturing PMIs (solid)

The ISM Manufacturing PMI rose to 48.4 in November, exceeding market expectations of 47.7 and up from October’s 46.5, marking the highest reading since June.

- Most notably, new orders rebounded after seven months of contraction (50.4 vs 47.1).

- Other key components showed improvements, with contractions in production (46.8 vs 46.2), employment (48.1 vs 4), and inventories (48.1 vs 42.6) softening.

- Price pressures eased (50.3 vs 8) and faster supplier deliveries (48.7 vs 52) supported the outlook.

The S&P Global US Manufacturing PMI was revised up to 49.7 from the preliminary 48.8 in November and up from October’s 48.5. This marks the highest reading since June and a near stabilization in the sector.

- A main driver was new orders declining only marginally, marking the slowest pace of contraction in five

- Business optimism surged, prompting renewed job creation after three months of cuts.

- However, production continued to be scaled back, citing hurricane-related disruptions, price increases and a lingering uncertainty from the pre-election period.

- Cost inflation eased to the lowest in a year, while output prices rose at a slightly faster pace.