Macro Flash Report

MANUFACTURING PMI

Takeaway:

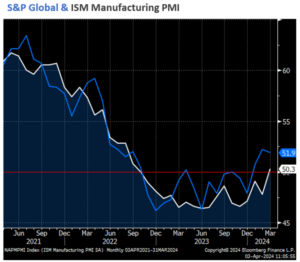

The contrast between March’s underwhelming Fed manufacturing surveys and the expansionary S&P and ISM manufacturing PMIs underscores the reality that, although the recent numbers are promising, the manufacturing rebound is still only in the early stages.

March’s ISM Manufacturing PMI surprised to the upside, beating market expectations of a rise to 48.4 from February’s 47.8, by jumping up to 50.3, signaling a return to growth for the sector after 16 months of contraction.

- The recovery is underscored by improved demand, as new orders increased (49.2 to 51.4) and new export orders holding steady at 6 and production saw a notable boost (48.4 to 54.6).

- Backlogs continued to be in moderate contraction at 46.3 and customers’ inventories contracted further (45.8 to 0), which is a level supportive of further production improvements.

- However, the sector still faces challenges, with employment (45.9 to 47.4), and a moderate increase in prices (52.5 to 55.8), which was mainly due to fluctuating commodity prices.

Overall, this highlights a cautiously optimistic turn in the manufacturing sector, driven by stronger demand and increased production, albeit with ongoing hurdles.

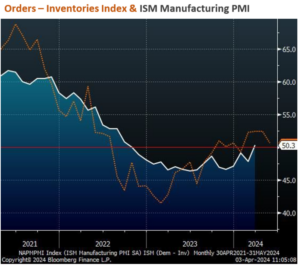

- The second chart shows the Orders – Inventories Index which combines different subcomponents of the ISM Manufacturing PMI. Historically is has been a good leading indicator for the upcoming trend. This index has been pointing to a slight expansion in the sector for 6 of the last 7 months.

The S&P Global US Manufacturing PMI final march data was adjusted down slightly to 51.9 from the preliminary figure of 52.5, reflecting a slight deceleration in growth from February’s 52.2. Despite this revision, the manufacturing sector remains in expansionary territory as it experienced its most significant growth in 22 months, propelling by improving economic conditions and market demand.

- This uptick led to an accelerated pace of manufacturing production and job However, the growth in new orders showed signs of slowing.

- Companies showed a tendency to reduce their inventories, resulting in decreased purchasing activities and reduced stocks of inputs and finished goods, reversing the increases seen in February.

- The period also saw a marked increase in both input costs and output prices, indicating rising inflationary pressures.

- Nevertheless, firms remained optimistic about the future, expecting continued output growth over the next year.