Macro Flash Report

February’s Fed Manufacturing Surveys

Takeaway:

Although the recovery in manufacturing has been slower than some expected, underlying dynamics suggest that we are on track for sustained expansion for the first half of 2025. Fed Manufacturing Survey data point to another expansionary print in the ISM Manufacturing PMI, due out on Monday, March 3rd.

Aggregate Fed Manufacturing Survey

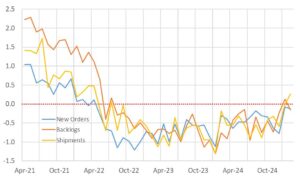

Primary Subcomponents

Richmond improved to 6 in February, surpassing the market expected -3 and up from -4 in the prior month. This marks the first expansion after 15 consecutive months of contraction.

- New orders stopped contracting (0 vs -4), while backlogs continued to deplete (-6 vs -5) allowing a sharp rebound in shipments (12 vs -9).

Kansas City remained unchanged at -5.

- The production index declined further to the lowest level in five months (-13 vs -9). Shipments (-11 vs -6) and new orders (-7 vs -6) slipped after rebounding last month.

- The future activity index eased slightly (14 vs 15).

Philadelphia eased to 18.1 from January’s notable 44.3 print, coming in slightly below the forecasted 19.4. However, although slowed, marks two consecutive months of strong expansionary readings.

- New orders (21.9 vs 42.9), shipments (26.3 vs 41), and backlogs (1.4 vs 24) all declined.

- Six-month expectations continue to see growth (27.8 vs 46.3), albeit were less widespread.

Dallas dropped to -8.3, retreating from the three year high of 14.1 in January. This represents the lowest level since August 2024.

- Production (-9.1 vs 12.2), company outlook (-5.2 vs 18.7), new orders (-3.5 vs 7.7), and capacity utilization (-8.7 vs 5) all took hits.

- Looking forward, expectations for activity remained optimistic but less so (7.7 vs 35.5).

NY Empire jumped to 5.7 in February from the drop to -12.6 in the previous month, and exceeding the expected -1.9. This signals a rebound in activity.

- New orders (11.4 vs -8.6) and shipments (14.2 vs -1.7) expanded once again. Prices paid increased at the fastest pace in nearly two years (40.2 vs 29.1).

- Firms continue to expect for conditions to improve, although lessened (22.2 vs 36.7).