Macro Report

This Week’s Takeaway:

This week’s data showed us that manufacturing activity has not yet rebounded, while housing continues to improve going into the traditional construction season. The labor market remains stable and has yet to signal meaningful cracks that would cause concern of a broader economic slowdown.

Notes:

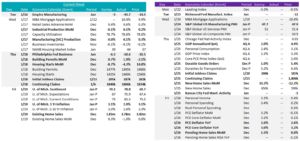

Manufacturing data provided a mixed view on the status of the recovery. The January readings for Empire (NY) & Philadelphia FED manufacturing surveys both came in below expectations, -43.7 vs -5, and -10.6 vs -6.5, respectively. The Empire print was concerning, with the lowest topline print since May 2020, while Philly showed a slight increase compared to the December print. Additionally, MoM December Industrial Production & Manufacturing Production indexes both printed slightly lower than November readings but above expectations, 0.1% vs -0.1%, and 0.1% vs 0.0%.

December Building permits and Housing starts both came in above expectations, 1.9% vs 0.7%, and -4.3% vs -8.7%. This was a strong signal of further activity, as the permits/starts relationship snapped back into sync. Although housing starts printed down compared to November, it is important to remember that this was a huge upside surprise. Additional signs of life come from the NAHB (Builders) Housing Market Index which printed up to 44 from 37 in January and above expectations of 39.

Although it remains below 50, this is the second straight month of increases. Existing home sales were the only raincloud on the week, printing -1% in December compared to 0.8% in November, and below expectations of 0.3%.

Initial and continuing claims both came in below expectations, 187k vs 205k, and 1,806k vs 1,840k, respectively. This is a clear signal that the labor market is cooling in a contained and controlled way, with initial claims down to their lowest level since September 2022.

Another impressive datapoint was the preliminary data for the University of Michigan Consumer Sentiment Survey printing 78.8 versus expectations of 70.1. If this reading holds when the remainder of the data is collected, this would be highest topline reading since July 2021. Looking more closely, expectations for 1yr inflation also improved, down to 2.9% versus 3.1% in December and “flat” expectations. This is a welcome sign after this index shot higher in October & November of last year.

Next Week’s Notes:

Next week’s data will provide insights into the manufacturing, industrial,

and housing sectors, as well as other economic indicators.

Both the Richmond and Kansas City FED Manufacturing Surveys for January will be released with no current market consensus on

expectations. January’s preliminary data for S&P Global US Manufacturing PMI is forecasted to slightly decrease to 47.7 from the prior month’s 47.9. For the industrial sector, December preliminary data for Durable Goods Orders is expected to show 1.0% growth MoM, down from 5.4% the previous reading.

The rest of the housing data for December will come in, with expectations of further improvements. New Home Sales MoM has current expectations of an increase to 10.2% from -12.2% the month prior, a significant up-tick. Meanwhile, Pending Home Sales MoM is also expected to increase, with market estimates of a rise to 1.5% from November’s stagnant 0.0%. These expectations are driven by the fact the 30yr Fixed Rate Mortgage steadily declined throughout the month of December, down over 55bps by most measures.

More data around inflation is anticipated, which will be the PCE Deflator YoY and the PCE Core Deflator YoY for December, with market estimates of the former remaining unchanged at 2.6%, and for the latter, a slight easing to 3.0% from 3.2% the prior month.

Finally, we will have an update on the weekly jobless claims data and a look into the overall growth of the economy from the Q4 GDP Annualized QoQ data, which has market expectations of 2.0%, down from the significant Q3 reading of 4.9%. The Atlanta FED GDPNow estimate suggests there is potential for another upside surprise in GDP, with the 01/18 update increasing to 2.4%.