Macro Report

Week’s Takeaway:

The broader economy showed additional signs of cooling from last year’s breakneck pace and the FOMC held rates steady.

Notes:

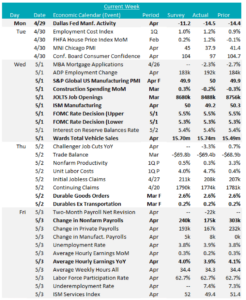

Ever since the current hiking cycle ended, the market has looked over “FED talk” and economic data with a fine-tooth comb, desperate to figure out when policy will start to ease. However, after 4 months of warmer than comfortable inflation readings and a Q1 GDP print that came in well below market expectations, this week’s meeting was going to be pivotal. The result was that the FOMC kept rates unchanged at 5.25-5.5% and Jay Powell’s press conference took more of a hawkish turn (both as expected, however, the latter did not fully satisfy market expectations). One of the more notable sticking points for why Powell drew his “hawkish line” below the threshold of the next rate move being a hike was because he noted that the committee viewed risks to their price/labor dual mandate more in balance than before. Plainly, this would suggest, they believe rates are sufficiently restrictive to bring inflation down while allowing the economy to continue growing and that an additional hike from here would do outsized damage to the labor market.

Now that we have the April jobs report and additional service sector data from the ISM, this underlying view received some support. Non-farm payrolls grew at a healthy, albeit lower meaningfully lower than anticipated pace, adding 175k jobs versus the expected 240k. Gains were broad based and Manufacturing payrolls added 8k versus the expected 5k, with March was revised down to -4k lost, versus the preliminary a “flat” reading.

As mentioned above, ISM Services PMI came in below expectations printing in contraction at 49.4 for the first time since December 2022.

This was driven by surging prices paid (59.2 versus 55, expected) and a deeper than expected contraction in employment (45.9, versus 49).

This week’s steel-specific data presented a mixed picture. For manufacturing, the final April S&P Global US Manufacturing PMI was a positive outlier, marginally increasing from the preliminary figure of 49.9 to 50. Conversely, the ISM Manufacturing PMI fell short of expectations, declining to 49.2 vs 50 from March’s 50.3, and similarly, the Dallas FED Manufacturing Survey disappointed, dropping to -14.5 vs an anticipated improvement to -11.2 from -14.4 in March. Overall, these figures

underscore the bumpy road to recovery. In the adjacent sector, March’s Construction Spending MoM also fell unexpectedly, marking the third month of negative growth by declining to -0.2% vs the projected 0.3% rise. This was primarily driven by a downturn in private spending being led by the residential segment shrinking by -0.7%, which offset the increase in public spending. Finally, and on a brighter note, April’s Wards Total Vehicle Sales exceeded expectations, jumping up to 15.74m from 15.49m vs the forecasted climb to 15.70m sales.

Next Week’s Notes:

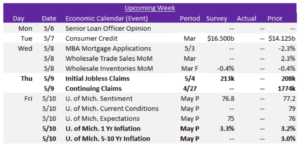

Next week’s economic data releases will be relatively light. We will see the weekly updates on Initial and Continuing Jobless Claims, with the former expected to rise slightly to 213k from 208k. Additionally, the preliminary May estimates for the University of Michigan consumer sentiment surveys will be reported. Market expectations for these include a forecasted increase in the 1-Yr Inflation expectations to 3.3% from 3.2%, and a decline in the Sentiment index to 76.8 from 77.2. These will be important to keep an eye on as they will provide insights into the trends of the labor market and inflation pressures.