Macro Report

Week’s Takeaway:

The big story for this week was the clear signal of stubborn and sticky inflation. As a result, the much-anticipated start to the rate cut cycle continues to be pushed back with the market currently pricing in the first cut in September.

Notes:

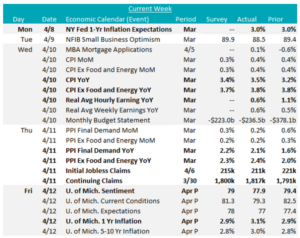

CPI YoY rose to 3.5% from February’s 3.2% and surpassed the forecast estimates of a 3.4% increase. At the same time, March’s CPI (Ex Food & Energy) YoY held steady at 3.8%, which was also above market expectations of 3.7%. Another concerning signal comes from Supercore CPI YoY which rose to 4.8%, it’s highest level since April 2024. In the run up of interest rates, Chair Powell specifically pointed to CPI Services (ex. Shelter) as a key indicator for where price pressure was trending.

The producer prices release, on the other hand, provided more of a mixed view on how upstream prices were coming in. Topline PPI YoY rose 2.1%, below expectations of a 2.2% level, while PPI ex. food and energy YoY came in slightly hotter, up 2.4% versus estimates of a 2.3% increase.

Moving on to the consumer, there are early indications that the bias towards disinflationary expectations is no longer as clear and pronounced. The March NY Fed 1-Yr Inflation Expectations, held steady at 3.0% (4th straight month) and the April preliminary University of Michigan 1-Yr Inflation Expectations rose back up to 3.1% from 2.9%, last month. The key risk here is that the longer inflation is sticky, the more likely we will see a surge in wages demanded as expectations for higher prices in the future are entrenched.

From the labor market side, real average weekly earnings YoY remained positive for the 10th straight month. Initial jobless claims came in below expectations again this week and those, coupled with the level for continuing claims point to a strong labor market.

Next Week’s Notes:

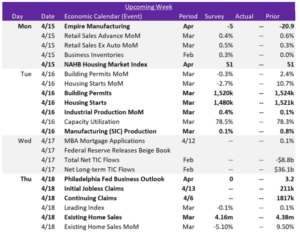

Next week marks the release of the initial batch of April Fed Manufacturing Surveys, with NY Empire projected to improve, with expectations for a rise to -5 from -20.9. Conversely, Philadelphia is anticipated to show a slight downturn, declining to 0 from 3.2.

Additionally, we will receive the Manufacturing (SIC) Production March figures, which is forecasted for a modest increase of 0.1%, a notable slowdown from February’s 0.8%, and March’s Industrial Production MoM, which is expected to show a more robust increase, with expectations for an increase to 0.4% from 0.1%.

Also, in the upcoming week, a slew of housing data will be released. The NAHB Housing Market Index is expected to stay stagnant at 51, indicating a neutral outlook among home builders. Additionally, we’ll see March’s Building Permits and Housing Starts, which are both anticipated for declines, dipping from 1,524k to 1,520k and from 1,521k to 1,480k, respectively. Finally, March’s Existing Home Sales is similarly expected for a slight slowdown, projected for a decrease to 4.16m from 4.38m.