Macro Report

Week’s Takeaway:

The labor market continues to surprise to the upside, while industrial sector data paints a mixed, albeit slightly optimistic view of February/March.

Notes:

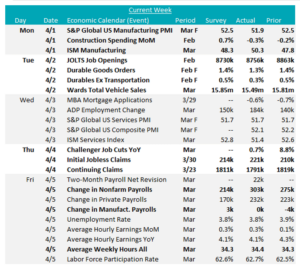

Arguably the most watched steel related economic data point came in significantly better than expectations. The ISM Manufacturing PMI surprised to the upside, printing 50.3, above expectations of 48.4. This marked the first expansionary print in 16 months. The S&P Global Manufacturing PMI also printed in expansion territory for the third straight month, albeit below expectations, at 51.9. This stands in contrast to very poor Fed Manufacturing surveys, which sharply reversed from their improving trend and pointed to contraction within the sector.

After last month’s upside surprise in Auto sales data, this month disappointed, with sales down to a seasonally adjusted annualized rate of 15.49M versus expectations of a slight increase to 15.85M.

Construction spending disappointed for the second straight month, with the total spending figure down -0.3%, versus expectations of a 0.7% rebound. Looking more closely, private residential spending continues to impress, up 0.7%. This was offset by a monthly decrease of -0.9% in private non-residential spending and the 1.2% decrease in public spending on the month caused the topline decline. Despite these monthly setbacks, the annual perspective offers a brighter outlook, with construction spending witnessing a robust 10.7% growth compared to the same month last year.

The latest job market data reveals several encouraging trends. The year- over-year increase in Challenger Job Cuts significantly slowed to 0.7% in March, down sharply from the 8.8% growth observed in February. In a surprising turn, the Change in Nonfarm Payrolls climbed to 303k, up from 275k in February, and well above the anticipated decline to 214k. However, the Change in Manufacturing Payrolls remained stagnant at 0, falling short of the expected increase to 3k and showing a slight recovery from the previous month’s decrease of -4k. Meanwhile, JOLTS Job Openings for February slightly declined to 8756k from 8863k but still managed to outperform forecasts, which had predicted a drop to 8730k. These figures indicate a resilient labor market, with positive momentum in employment despite some areas of softening.

Next Week’s Notes:

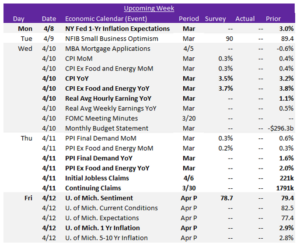

Next week provides an updated view of inflation trends with the March data. The CPI YoY has market expectations of rising to 3.5% from 3.2%, while the CPI (Ex Food & Energy) YoY is forecasted for a slight decline from 3.8% to 3.7%. Additionally, we will delve into March’s PPI Final Demand YoY and the PPI (Ex Food & Energy) YoY, alongside with the NY Fed 1-Yr Inflation Expectations.

This upcoming week also brings a preview of April through the University of Michigan consumer surveys preliminary figures. The topline figure printed at its highest level since July 2022 in March and has been showing encouraging signals that consumer expectations on inflation remain in line with the FED target. It is currently expected to slightly soften to 78.7 from 79.4.

Another important signal for inflationary pressure will come from March’s Real Avg Hourly Earnings YoY. To date, the red-hot labor market has not resulted in a wage-price spiral, which was one of the closely watched upside risks as inflation started rolling over. The current market theory that immigration has been a significant contributor to discrepancies in the household survey and establishment payrolls also supports the theory that a wage-price spiral is not a top risk for reaccelerating price pressure.

Also, we will get the updated Initial and Continuing Jobless Claims, which have been one of the most consistent indications of labor market stability.