Macro Report

Week’s Takeaway:

There was no clear theme in this week’s data, however, we continue to see signs that the labor market, and inflation are running hotter than the FED would have hoped. On top of that, the overall economy continues to grow at an impressive rate. It is becoming increasingly unlikely that we will see the number of rate cuts the market is currently pricing in.

Notes:

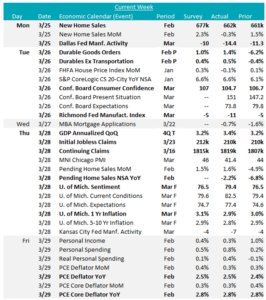

4Q23 GDP revised higher, driven by more robust consumer spending, which appears to remain strong well into the first quarter, with real personal spending from (PCE Report) up 0.4% in February. Looking more closely at that report, the Topline and Core PCE prints came in line with expectations, at 2.5% and 2.8%, respectively. Both continue to trend lower but are above the Fed target. It is important to note that the disinflationary base effect which encouraged markets that prices were under control will start to subside once we have cleared the summer months and will start to be a hurdle in getting PCE to 2%.

March’s Fed manufacturing surveys disappointed compared to market expectations and showed overall declines across the board. There were signals of a burgeoning recovery in the first two months of the year. This move appears to be a cautionary tale for optimism driven solely by hopes of impending interest rate cuts, when you dig into the commentary.

Housing data was mostly stable this week, after significant upside surprises in last week’s data for the sector. New home sales were only down slightly at 662k, compared to January and slightly below expectations. While pending home sales were up 1.6%, beating expectations of a 1.5% increase.

The Headline University of Michigan Consumer Sentiment Survey printed at its highest level in 32 month, more than 2.5 years at 79.4. The most encouraging signal from the data is that inflation expectations came in below the initial estimate for both the 1-year and longer-term periods.

Next Week’s Notes:

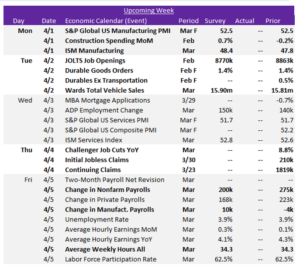

Next week, we are set to gather the comprehensive data from the beginning of the month, which will provide valuable insights across the manufacturing, construction, and automotive sectors, alongside a slew of labor market measures.

For the manufacturing sector, we will receive some important updates. The final March S&P Global US Manufacturing PMI is projected to remain steady at the preliminary results of 52.5 and March’s ISM Manufacturing PMI is forecasted to experience an increase to 48.4 from February’s 47.8, both indicating stable and slight improvements for the sector. Additionally, we will also review the final February figures for Durable Goods Orders and Durables Ex Transportation, which are anticipated to confirm the preliminary data’s upside surprises.

In the upcoming week, February’s Construction Spending MoM will be published. Market expectations are for 0.7% growth, a significant recovery from the previous month’s -0.2% decline – the first monthly contraction in construction activity since December 2022, which was primarily driven by a -0.9% drop in public construction spending.

March’s Wards Total Vehicle Sales figures will be released and is anticipated to show a rise to 15.9m, up from the previous month’s 15.81m, suggesting a continuation of growth in the auto sector.

In the upcoming reports, we will delve into a set of labor market data, which will provide a detailed snapshot of current labor market trends. February’s JOLTS Job Openings are expected to decrease to 8770k from January’s 8863k. Similarly, March’s Change in Nonfarm Payrolls are projected to show a slight decline, falling to 200k from 275k. In contrast, March’s Change in Manufacturing Payrolls are forecasted to rebound, rising to 10k after a decline of -4k the previous month. Moreover, March’s Average Weekly Hours are anticipated to hold steady at 34.3 hours. We will also receive the Challenger Job Cuts YoY March figures, as well as the weekly update for Initial and Continuing Jobless Claims.