Macro Report

Week’s Takeaway:

This week’s data showed mixed results from Fed manufacturing data, further softness on the housing side, and a better-than-expected inflation print.

Notes:

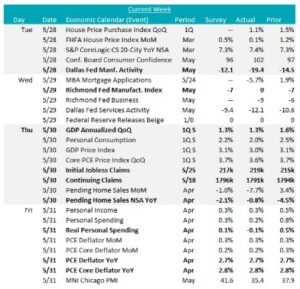

The FED Manufacturing survey provided opposing signals. Dallas printed down to -19.4, below an expected uptick at -12.1. Richmond, however, came in above expectations, printing 0, versus and expected -7. Now that we have all the Fed surveys, our expectation is that the ISM Manufacturing PMI for next week would tick higher but remain in slightly contraction territory, matching overall market expectations.

Pending home sales (NSA YoY) in April continued the recent trend of negative prints, but came in slightly better than expectations, down 0.8%. From the affordability side mortgage rates remain high and all this week’s measures of home prices continued to increase.

Finally, the Core PCE Deflator came in below expectations, with the YoY print down to 2.75%, from 2.81% in March. This is a welcome signal given the uptick in CPI, but more substantial progress will have to be made over the next two months before the data starts to see a worsening base effect. Because of this, FED Officials will likely continue to say more evidence is needed before interest rate cuts begin.

Next Week’s Notes:

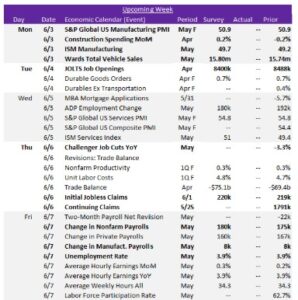

Next week, we will receive the first-of-the-month data, starting with sector-specific information. For the manufacturing sector, May’s S&P Global US Manufacturing PMI is expected to remain steady at 50.9, while May’s ISM Manufacturing PMI is anticipated to increase slightly to 49.7 from April’s downside surprise of 49.2. In the construction sector, April’s Construction Spending MoM is forecasted to grow by 0.2%, up from March’s downside surprise of -0.2%. Additionally, the auto industry will be updated with Wards Total Vehicle Sales, which are expected to rise to 15.80m from April’s 15.74m sales. These insights suggest slight improvement and stability across these steel end-user sectors.

We will also receive a slew of labor market data in the upcoming week. April’s JOLTS Job Openings is expected to decline to 8400k from 8488k. May’s Challenger Job Cuts YoY will be released, along with Change in Payrolls. Nonfarm Payrolls are anticipated to rise slightly to 180k from 175k, while Manufacturing Payrolls are expected to be unchanged at 8k. The Unemployment Rate is forecasted to stay stagnant at 3.9% for May, and the weekly update for Initial and Continuing Jobless Claims have the former projected to rise to 220k from the previous 175k reading. These insights provide a mixed but relatively stable outlook for the labor market.