Macro Report

Week’s Takeaway:

This week’s industrial and labor market data came in below expectations, while the FOMC clearly opened the door for rate cuts in September.

Notes:

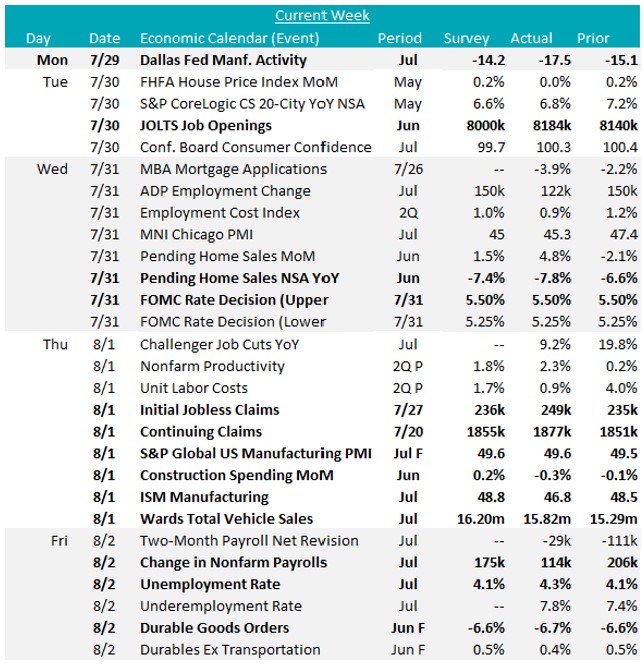

This week’s most notable data release was the unexpected drop in the ISM Manufacturing PMI, which fell to 46.8 against a forecasted improvement to 48.8. This decline followed another surprise in the manufacturing sector, with the Dallas Fed Manufacturing Survey worsening to -17.5 instead of the anticipated rise to -14.2. On a slightly positive note, the final results for the S&P Global US Manufacturing PMI saw a minor uptick, reaching 49.6 from the preliminary 49.5.

In other steel-specific sectors, Construction Spending disappointed, declining by -0.3% in June compared to May’s- 0.1% and missing the expected 0.2% increase. Wards Total Vehicle Sales rose to 15.82m from June’s 15.29m, although was below the projected 16.20m sales. Additionally, the final data for June’s Durable Goods Orders aligned with preliminary results, showing a -6.6% decline. Lastly, Pending Home Sales NSA YoY decreased by -7.8% in June, falling short of the forecasted -7.4% and down from May’s -6.6% drop.

The batch of labor market data reported this week indicated a further cooling to the recent trend. The Unemployment Rate rose to 4.3%, surpassing expectations of holding steady at 4.1%, marking the fourth consecutive month of increases and the highest rate since October 2021 (officially triggering the Sham rule). Change in Nonfarm Payrolls added 114k jobs, notably below June’s 206k and the forecasted 175k. This is the lowest level in three months and under the average monthly gain of 215k over the past year, signaling a cooling labor market. Conversely, JOLTS Job Openings increased slightly in June, rising to 8184k from 8140k, exceeding the anticipated 8000k, continuing to trend towards 2019 levels. Additionally, both Initial and Continuing Jobless Claims came in above projections, 249k vs 236k and 1,877k vs 1,855k, respectively.

The FOMC Rate Decision was to hold FED Funds at 5.25-5.5%, but opened the door for interest rate cuts in September (all as the market expected) the subsequent weak data over the last two days all but locked in the fact that long awaited cutting cycle is about to begin.

Finally for the week, the FOMC Rate Decision met market expectations, holding rates at 5.25-5.50%, reflecting a cautious approach amidst a cooling labor market and a disappointing industrial sector. However, supporting expectations for an interest rate cut in September.

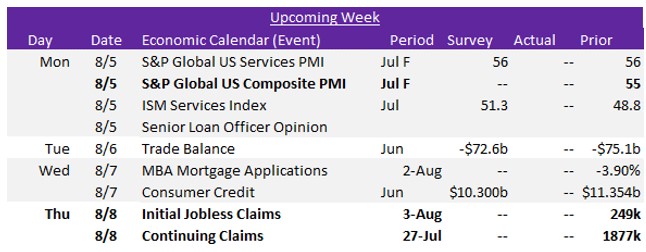

Next Week’s Notes:

Next week will be light on data releases, with the primary focus on July’s final data for the ISM Services and Composite PMI. Additionally, the weekly updates for Initial and Continuing Jobless Claims will be reported. These indicators will provide valuable insights into the service sector’s performance and the current state of the labor market.