Macro Report

This Week’s Takeaways:

Economic data continues to surprise to the upside with labor market data, auto sales, and construction spending all showing resilience and growth. Our view of this is higher confidence in a soft landing, rather than an increased risk of a November interest rate hike.

Notes:

After recent labor market data indicated a cooling landscape, nearly all the data from this week beat expectations and reversed that slowing trend. A superficial interpretation of this could lead market observers and participants to believe that the Fed will opt for an additional 25bps rate hike, however, wage data which has more meaningful inflationary repercussions remains restrained.

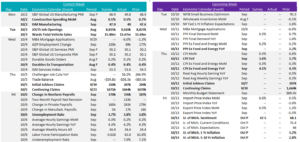

- The Change in Nonfarm Payrolls was red-hot and shows 336k jobs added in September (up from 227k in August), and a prior two months revision of an additional 119k.

- JOLTS Job Openings were well above expectations as well, up 783k to 9.6M, versus expectations of a slight decline.

- Finally, Initial and Continuing Jobless Claims moved very little, but both were below expectations. Both remain in a downtrend since the summer.

September ISM Manufacturing PMI beat expectations coming in at 49.0, this was up from 47.9 in August and highest level in 10 months, but it remains slightly in contraction territory. Underlying dynamics from the demand components indicate that we could start seeing expansion in this sector before the end of this year, after 11 straight months of contraction.

August Construction Spending continues to show resilience in a high interest rate environment, with total spending at expectations of a 0.5% MoM increase. This was primarily driven by residential spending which continues to rebound – up 0.6% on the month but still -3% compared to last year. Non-residential spending, while losing steam increased further this month as well, up another 0.4% compared to July and up 17.6% compared to last year. The forwarding looking ABI (Architectural Billings Index) suggests that the next 9 months of non-residential spending will show further deceleration but not a meaningful collapse.

Next Week’s Notes:

The PPI (ex. food and energy) YoY has been on a downward trend since reaching record high of 9.2% in March 2022, with the August data hitting 2.2%. The PPI that will be released this week is expected to increase slightly to 2.3%, indicating that this downward trend has moderated.

Core CPI (ex. food and energy) YoY has been decreasing since March 2023, with August data declining to 4.3% from 4.7% the prior month, the lowest it has been since September 2021. This week’s data that will be release expect CPI to continue this downward trend, hitting 4.1%. This suggests that inflationary pressures are persisting on their trend of easing up.

After a significant decrease seen in early September Initial Jobless Claims have been steadily increasing again, with market expectations for this week to be at 210K. On the other hand, Continuing Claims has been on a slight decline, despite market expectations of an increase. This week’s data is expected to show another slight decrease, indicating that the labor market is still at tight levels. Risk is more skewed to the upside with ongoing UAW strikes and a potential government shutdown in the months ahead.