Macro Report

Week’s Takeaway:

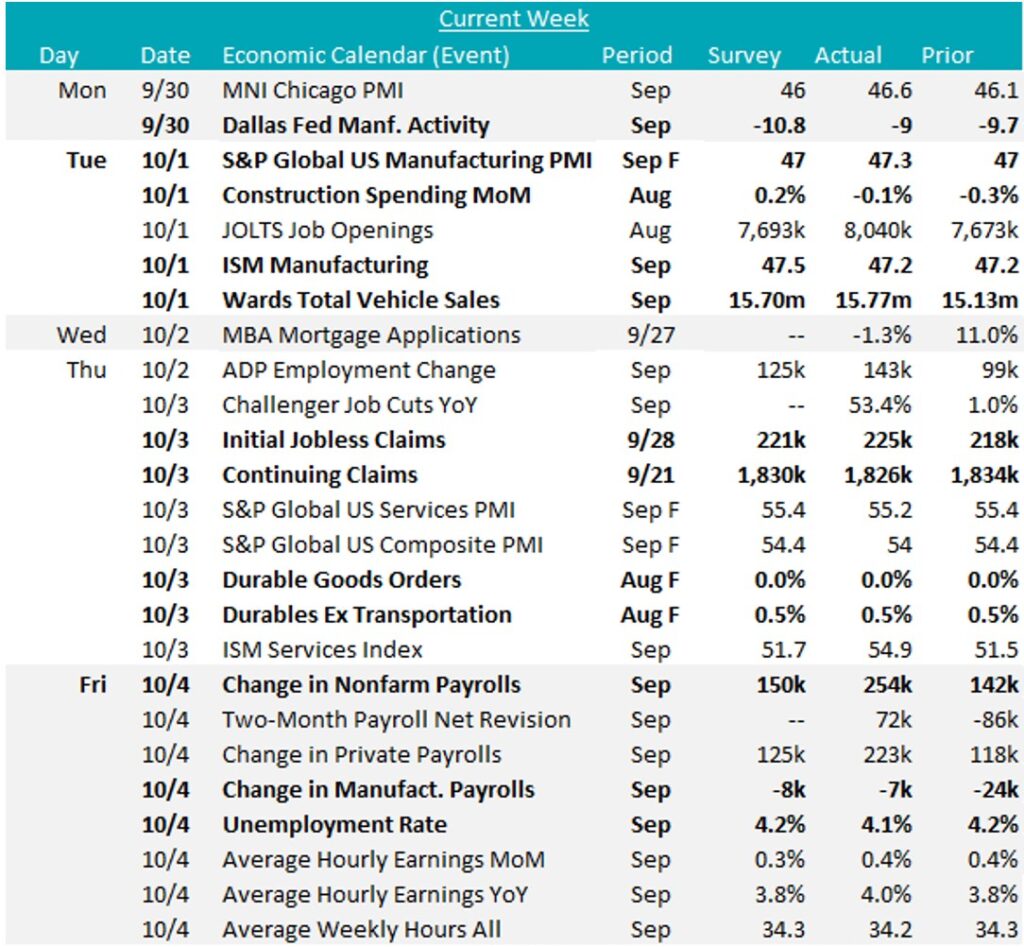

Much awaited industrial data came in muted this week, while significantly better than expected labor market data will temper expectations of a rapid rate cutting cycle.

Notes:

September manufacturing data from early in the week underscore continued contraction within the sector. The summation of:

- FED Manufacturing surveys (slightly higher still in contraction)

- ISM Manufacturing PMI (flat MoM at 47.2, below expected 47.5)

- S&P Global Manufacturing PMI (up 47.3, above expectations for a flat print at 47)

all highlight the fact that elevated borrowing costs and election uncertainty have stood in the way of a recovery in consumption from the sector. The FED will clearly continue the cutting cycle from here, but this week’s labor market data puts to question whether it will be as rapid as the market was pricing.

On the construction spending side, August CPIP (Construction Put In Place) shows a continued 4.1% YoY strength, however, recent monthly figures are pointing to stagnation, down (-0.1% versus an expected 0.2%) for the 3rd consecutive month with 6 of the last 7 coming in below expectations. Private spending decreased by 0.2%, and nonresidential spending was down 0.1%. On the other hand, public spending continues to be a bright spot, up 0.3% this month for the 6th time in the last 8.

Of most note, labor market data has recently been signaling more resilience than previously thought. This starts with initial jobless claims, which since the end of July have been in a clear downtrend (signaling a reduced rate of firing). Additionally, JOLTS job openings unexpectedly rebounded back above the 8M level to 8.04M in August, rather than continuing their downtrend toward the 2019 average of 7.15M (increased labor demand). All culminating to a red-hot September 254k addition to Nonfarm payrolls, well above the expectation of 150k job added. Furthermore, the unemployment rate fell to 4.1%, down from August’s 4.2% and expectations for an unchanged print. The market reaction was a clear reset in how rapid the FOMC is going to cut rates going forward.

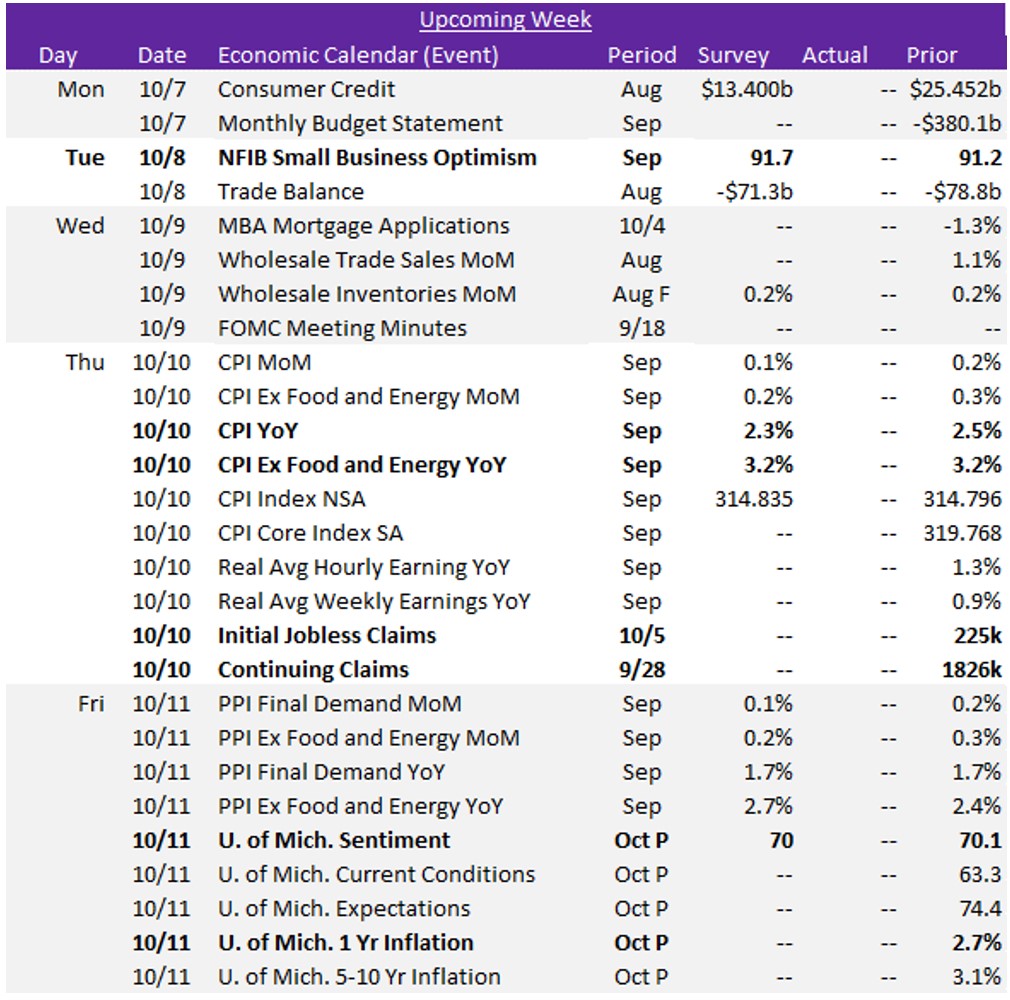

Next Week’s Notes:

Next week, key macroeconomic indicators will be reported that will provide insights into current economic conditions.

First, the NFIB Small Business Optimism index for September is expected to rise to 91.7 from 91.2, suggesting a slight increase in confidence among small business owners, potentially signaling a positive outlook for economic growth.

Additionally, inflation data will be released, with the Consumer Price Index (CPI) YoY for September projected to decrease to 2.3% from 2.5%. The CPI (Ex Food & Energy) YoY is anticipated to remain steady at 3.2%. Preliminary results from October’s University of Michigan consumer surveys will also be available, with the Consumer Sentiment index expected to slip slightly to 70 from 70.1 in September. These market expectations for CPI to see further easing and stability, while the forecasted slight dip in consumer sentiment suggest that, although consumers remain cautious, there are no immediate concerns about rising prices.