Macro Report

Week’s Takeaway:

This week’s data showed another week of increased optimism for activity in the future, but soft current data. The shift in expectations for lower near-term/higher long-term inflation is notable when considering the FED’s next couple meetings.

Notes:

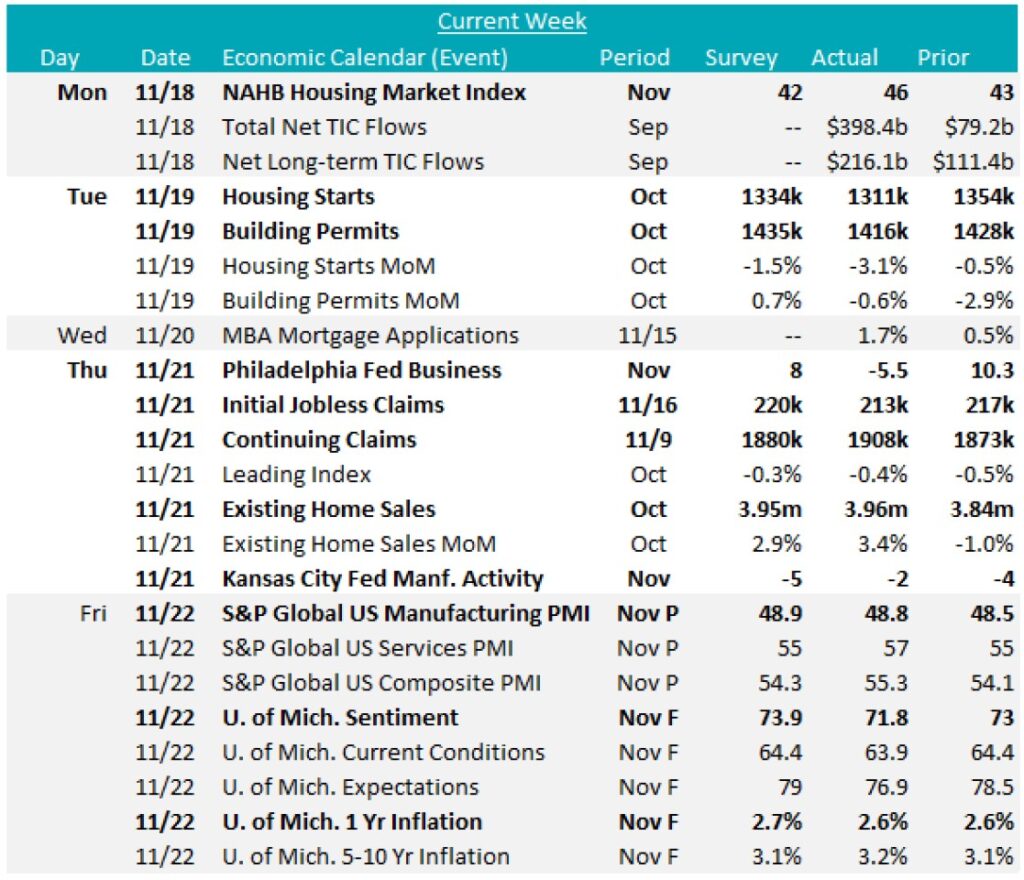

On the industrial side, November data signaled a further contraction in activity from both of this week’s Fed Manufacturing Surveys. Philadelphia was the more disappointment print at -5.5, coming in worse than the anticipated print lower from 10.3 to 8. Kansas City on the other hand was slightly more optimistic, coming in at -2, which while still in contraction territory is better than the expected -5. Furthermore, while the preliminary S&P Global US Manufacturing PMI increased to 48.8, it remains in contraction territory and was slightly below the expected 48.9.

Housing sector data presented an optimistic outlook for the future, while current activity remains hampered by the rise in mortgage rates. There was improved optimism among homebuilders, with the NAHB Housing Market Index rising to 46 in November, surpassing expectations of a decline to 42 to reach the highest level in seven months. However, October’s Housing Starts and Building Permits both fell short of forecasts, with Starts at 1,311k vs the expected 1,334k and Permits at 1,416k vs the expected 1,435k. Meanwhile, Existing Home Sales for October increased to 3.96m, slightly exceeding the anticipated 3.95m.

Finally, the final University of Michigan Consumer Sentiment Survey for November rose to 71.8 from 70.5 MoM. While the final data came in below the preliminary estimate it is a clear signal of optimism following the election. Another dynamic that deserves attention is the shift in inflation expectations. After 1yr inflation expectations remained stubbornly high for most of the year, the last 3 months have provided a promising signal of lower expectations – this culminated in todays data, where the figure came in at 2.6%, down from last months print at 2.7%. On the other hand, the longer-term inflation expectations jumped from 3% to 3.2%, matching this cycle’s all-time high from November 2023. This shift was mirrored by the market’s immediate reaction to Trump’s victory, where longer-term yields rose more significantly than the near-term. This clearly signals a shift towards higher expectations of growth over Trump’s administration, but also an increased risk of resurgent inflation which has yet to be fully trounced.

Next Week’s Notes:

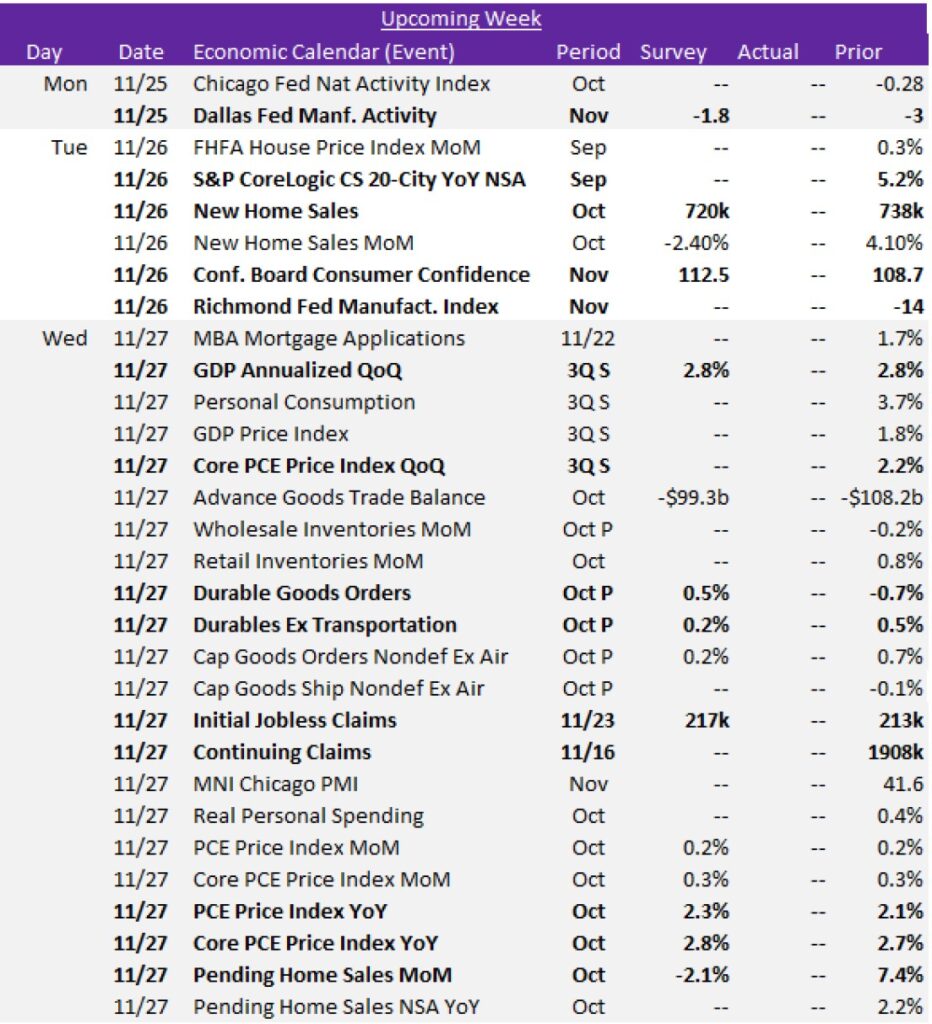

Next week, key manufacturing, housing, and macroeconomic data will be released, providing insights into economic conditions and steel demand.

For the manufacturing sector, the final two November Fed Manufacturing Surveys will be issued: the Dallas index, expected to improve to -1.8 from October’s -3, and the Richmond index. Additionally, the preliminary results for October’s Durable Goods Orders is forecasted for a 0.5% increase, which would be a rebound from -0.7% in September. Durables Ex Transportation is anticipated to rise by 0.2% from 0.5% in the prior month.

In housing, New Home Sales for October are projected for a decline to 720k from 738k, while Pending Home Sales MoM is estimated to experience a -2.1% fall, which would be a notable drop from September’s 7.4% increase. These market expectations suggest that housing sales may be facing some headwinds.

On the macroeconomic front, GDP for Q3 is forecasted to hold steady at 2.8%. November’s Conference Board of Consumer Confidence is anticipated to jump up to 112.5 from 108.7, which would reach the highest level since July 2023. The Fed’s preferred measure of inflation, the Personal Consumption Expenditure (PCE) Price Index report for October will be published, with PCE YoY expected to rise to 2.3% from 2.1%, while Core (Ex Food & Energy) PCE YoY is forecasted to tick up to 2.8% from 2.7%. Finally, we will receive the weekly updates on Initial and Continuing Jobless Claims, with Initial Claims projected to inch up to 217k from 213k. These forecasts indicate resilience and optimism in the economy despite expectations for sticky inflation.