Macro Report

Week’s Takeaway:

This week showed that inflationary pressures are proving more persistent than previously anticipated. Coupled with a stronger-than-expected industrial production reading, these developments suggest the Federal Reserve will likely continue to pause the cutting cycle in the near term.

Notes:

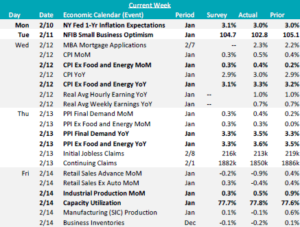

January Industrial Production data surprised to the upside, increasing by 0.5% month-over-month, surpassing the forecasted 0.3%, with Capacity Utilization ticking up by 77.8% (vs 77.7%) from December’s 77.6%. This points to resilience in the sector, signaling that demand may be holding steady. However, Manufacturing (SIC) Production missed expectations, declining by -0.1%, compared to the anticipated 0.1% increase, following December’s 0.6% rise, suggesting that the manufacturing sector is still facing some challenges.

The main event this week was the inflation data, which came in hotter than expected. The Consumer Price Index (CPI) YoY for Core increased by 3.3%, vs the expected 3.1%, and the Topline rose by 3.0%, exceeding the 2.9% forecast. While seasonal factors and base effects played a role, this acceleration in inflation suggests that the previous disinflationary trend has stalled for now. Similarly, the Producer Price Index (PPI) YoY for Core rose by 3.6%, vs the anticipated 3.3%, and the Topline advanced by 3.5%, surpassing the forecasted 3.3%. These results indicate that inflation remains sticky, making limited progress toward stabilization ahead of expected tariff implementations. The strong inflation data significantly reduced the likelihood of multiple interest rate cuts by the Fed this year.

Lastly, on the sentiment front, the January NFIB Small Business Optimism index fell short of expectations, falling to 102.8 vs 104.7 from December’s multiyear high of 105.1. This revealed some cautiousness around future activity as uncertainty resurged. Additionally, the NY Fed 1-Year Inflation Expectations for January held steady at 3.0%, beating the forecasted increase to 3.1%, suggesting that consumers’ outlook on inflation remains relatively stable.

Next Week’s Notes:

Next week will bring important data releases for the manufacturing and housing sectors, along with a consumer sentiment report.

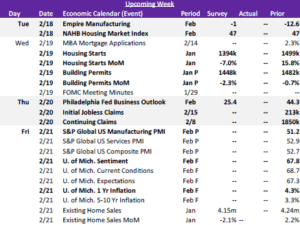

In manufacturing, we will receive the first two of five February Fed Manufacturing Surveys: the NY Empire index, which is expected to improve to -1 from -12.6, and the Philadelphia index, forecasted to ease to 25.4 from 44.3. Additionally, the preliminary results for February’s S&P Global US Manufacturing PMI will be reported. These will provide the first insights into the sector’s health for February.

For the housing sector, January’s Housing Starts and Building Permits are both anticipated to show declines. Starts are forecasted to fall to 1394k from 1499k and Permits are expecting a slip to 1448k from 1482k. January’s Existing Home Sales are also anticipating a decrease, declining to 4.15m from 4.24m in February. Also, the NAHB Housing Market Index for February is expected to hold steady at 47, signaling cautious sentiment in homebuilders. These market expectations suggest some cooling in the sector.

Finally, the University of Michigan consumer surveys final results for February will be released, providing updated insights into consumer confidence and expectations, which preliminary estimates showed some tempering.