Macro Report

Week’s Takeaway:

This week provided further encouraging data on the rebound in manufacturing, while an especially cold January froze out housing activity. Consumer concerns around upcoming inflation continue to accelerate.

Notes:

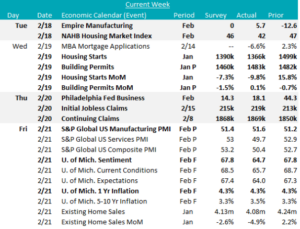

Early January Fed Manufacturing Surveys are continuing to point to early stages of a rebound in activity. Empire (NY) came in at 5.7, above the expected increase to 0. Philadelphia also came in at 18.1, better than the expected print at 14.3. New orders and shipments were primary drivers of this action, while employment contracted for both. Additionally, the preliminary S&P Global US Manufacturing PMI came in slightly better than expected (51.4), increasing to 51.6.

Housing data provided a mixed outlook, with building permits increasing 0.1% and clearly signaling further runway for builders, while housing starts fell 9.8% due largely to an unseasonably cold January. This was further confirmed by the NAHB Housing Market Index which printed at 42, a 5- month low, well below the expected slight decline to 46. The primary factor there, was a souring in expectations, which fell 13 point to 46 – the lowest reading since December 2023. Finally, existing home sales fell more significantly that expected, declining 4.9% to 4.08M.

Finally, the final University of Michigan Consumer Sentiment Survey was released and painted a pessimistic picture after initially improving after President Trump’s victory in November. The main takeaway is significant concern around inflation. The 1yr Inflation Expectation held steady at 4.3%, while the 5-10yr Expectation ballooned to 3.5%, the highest reading since 1995. Coincidentally, 1995 is the only time a soft landing was successful following prolonged restrictive interest rate policy. With all of this in mind, we continue to believe that the FOMC will not be cutting interest rates this year.

Next Week’s Notes:

Next week, several key data releases will provide insights into the manufacturing and housing sectors, as well as broader macroeconomic trends.

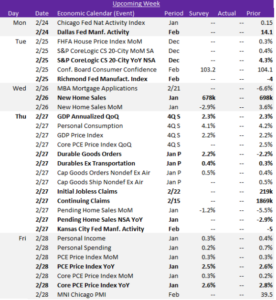

The final three of five February Fed Manufacturing Surveys will be released: the Dallas, Richmond, and Kansas City indexes. Additionally, preliminary January results for Durable Goods Orders will be reported, with expectations of a 2.2% month-over-month increase, reversing the previous month’s -2.2% decline. Durables Ex Transportation is anticipated to rise by 0.4%, up from a 0.3% increase in December.

In the housing sector, data on New Home Sales will be released, with January sales expected to decline to 678k from 698k in December. We will also receive the January Pending Home Sales report. Furthermore, the S&P CoreLogic Case-Shiller 20-City Index for December will provide insights into housing prices.

For broader economic indicators, the updated estimate for Q4 GDP will be published, with market expectations for it to remain unchanged at 2.3%. The January Personal Consumption Expenditure (PCE) report will also be released, the Fed’s preferred gauge of inflation. The PCE YoY is anticipated to tick down to 2.5% from 2.6%, while the Core (Ex Food & Energy) PCE YoY is expected to edge lower, declining to 2.6% from 2.8% in December.