Macro Report

**Flash Report – ISM Manufacturing**

Takeaway:

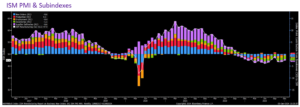

The December ISM Manufacturing Report underscores a prolonged contraction in the US manufacturing sector, now in its 14th consecutive month. Despite this downturn, primarily driven by weaker orders, there were signs of some resilience, with a notable increase in production and the PMI beating expectations. Overall, the data reflects a challenging period for the industry, yet with emerging indications of early stabilization.

December Data:

Manufacturing PMI rose by 0.7 to 47.4, beating market expectations of an increase to 47.1 from 46.7.

New Orders continued to contract, with the Index falling to 47.1. Backlog of Orders showed some improvement but remained in contraction, rising from 39.3 to 45.3.

There was a positive note with the Production Index increasing to 50.3, breaking into expansionary territory. Employment in the sector is still contracting, although the rate of contraction has slowed, going up from 45.8 to 48.1. Supplier Deliveries have become faster, indicating less pressure on supply chains.

Both Inventories and Customer Inventories contracted, suggesting there still is some cautiousness in response to demand uncertainty.

Prices are decreasing, down to 45.2 from 49.9. However, there are increases in the steel and aluminum markets.

Both Exports and Imports are still contracting, although both saw improvements, with new export orders rising to 49.9 from 46.0 and imports slightly rising to 46.4 from 46.2 the month prior.

None of the six largest manufacturing industries registered growth in December, reflecting widespread challenges across the sector.

Looking forward, the report includes mixed signals about the future. Some respondents anticipate an increase in manufacturing activity due to anticipated capital investments, while others forecast a slow year. Either way, there will be some challenges in 2024.