Fundamental Report

Supply-Side Takeaway:

The U.S. HRC price fell below adjusted Global pricing and both moved under $700 for the first time since December of last year. The supply side is restricted, this is seen in extended lead times driven by the Granite City idling and quiet extensions on maintenance outages. Furthermore, import arrivals remain surprisingly subdued given the increased domestic-global price differential from earlier in the year. The primary upside risk going into Q4 is that the market continues overreacting to an ongoing auto-strike while consumption from other sectors outperform expectations.

Notes:

- The global HRC price was down again this week, and it has not increased by more than 4% in 28 weeks. The current spread between the U.S. and global HRC price decreased by $24 and went negative for the first time since the beginning of February.

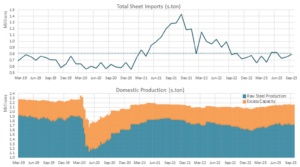

- September import data suggests that sheet arrivals will remain subdued at 796k short The current projection is just below the Post-232 pre-pandemic average of 810k tpm which suggests they are in neutral territory.

- Capacity Utilization ticked higher last week, up 1% to 76.3%, translating to 1.735M tons per week of raw steel production.