Macro Report

Week’s Takeaway:

This week, although light on data, offered some reassurance as the service sector remained resilient and the labor market, while cooling, showed signs of stabilizing at a manageable pace.

Notes:

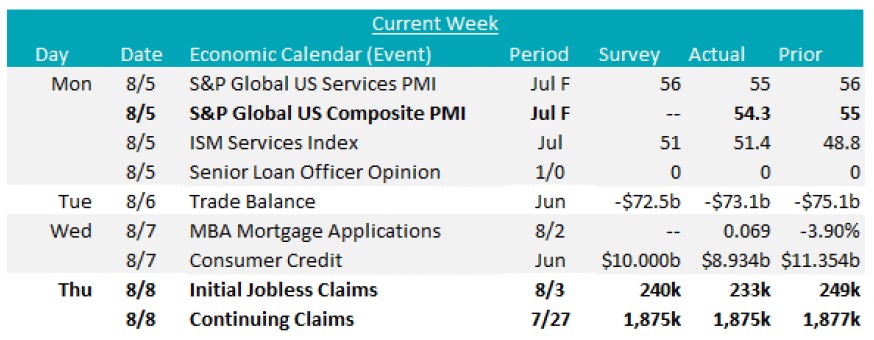

Initial Jobless Claims dropped by 17k to 233k versus the market expected 240k, marking the largest decline in nearly a year. This follows the previous week’s upwardly revised figure of 250k, which had been the highest in a year, easing some concerns about the labor market cooling too rapidly.

Meanwhile, Continuing Jobless Claims increased by 6k to 1875k, the highest since November 2021.

The S&P Global US Composite PMI was revised down to 54.3 in July from a preliminary estimate of 55, showing a slight decrease from June’s 54.8.

Despite the revision, the reading still indicates solid monthly expansion in private sector business activity, primarily driven by the service sector. The S&P Global US Services PMI was revised lower to 55 from a preliminary 56, compared to 55.3 in June. Although the rate of growth in the services sector eased slightly, the reading continues to point to robust expansion, with new business rising for the third consecutive month at a solid pace.

Next Week’s Notes:

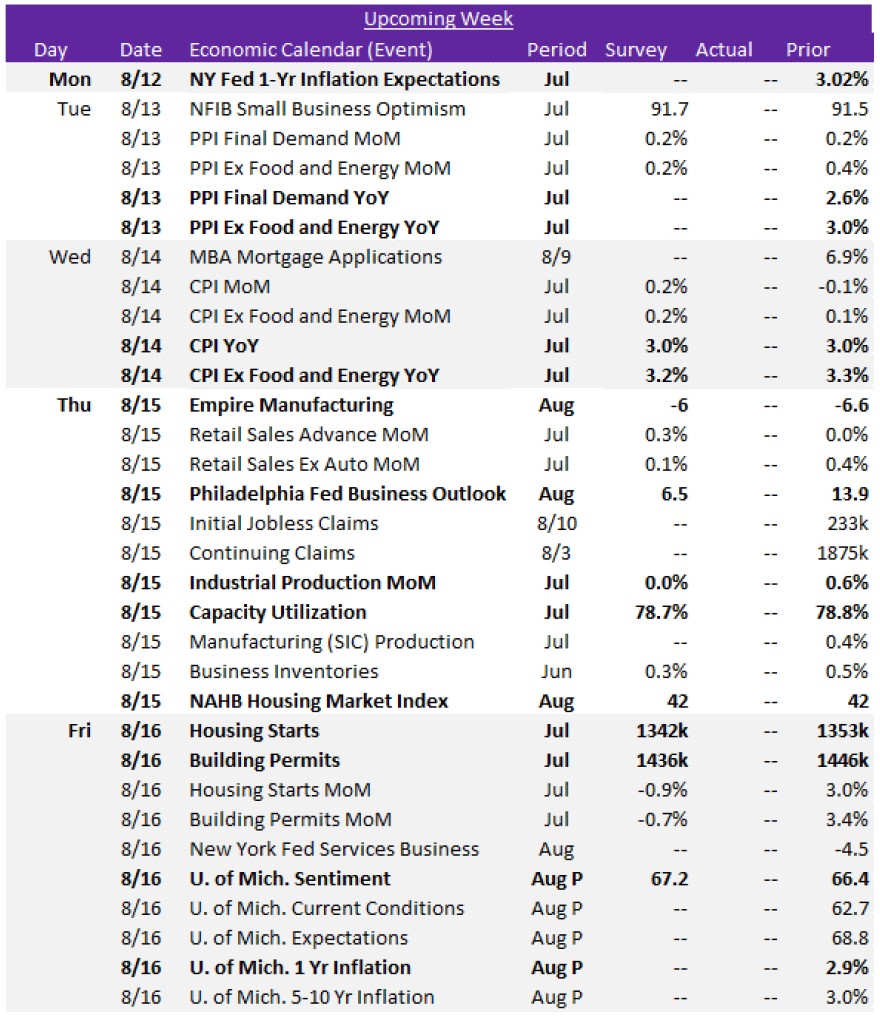

Next week, the upcoming data releases will provide key insights into the state of the manufacturing and housing sectors, as well as inflation trends, all of which will be critical in shaping market expectations and the Fed’s monetary policy decisions.

In manufacturing, the first two August Fed Manufacturing Surveys will be released. The NY Empire Index is expected to improve slightly to -6 from – 6.6, while the Philadelphia Index is forecasted to decline to 6.5 from 13.9. Industrial Production MoM is anticipated to remain flat at 0.0%, down from June’s 0.6% increase, with Capacity Utilization projected to tick down slightly to 78.7% from 78.8%.

The housing market will also be in focus, with July’s Housing Starts and Building Permits both expected to decline. Housing Starts are forecasted to drop to 1342k from 1353k and Building Permits are projected to decrease to 1436k from 1446k. The August NAHB Housing Market Index is expected to hold steady at 42.

Finally, a batch of inflation data for July will be released. CPI YoY is forecasted to remain at 3.0%, while Core CPI (Excluding Food & Energy) YoY is projected to slip slightly to 3.2% from 3.3%. July’s PPI data will also be released, along with the NY Fed 1-Year Inflation Expectations.

Additionally, we’ll get our first look at August’s inflation expectations through the preliminary results of the University of Michigan consumer surveys.