Fundamental Report

Supply-Side Takeaway:

Imports and domestic production have yet to materially subdue, while the domestic – global differential flipped positive. With limited room to the downside, the quickly approaching substantial maintenance outages could be a meaningful catalyst.

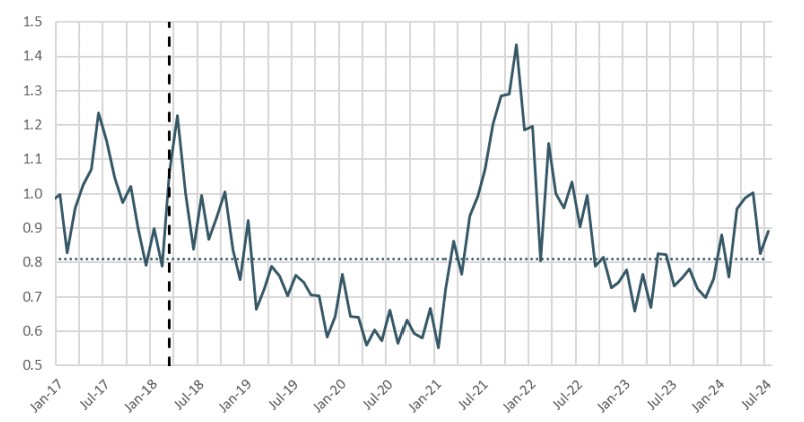

Imports and the Domestic – Global HRC price differential expanded further, turning positive after remaining negative for six weeks. The move was the result of the domestic spot price rising, while the global average price continued to slip. On the imports side, we got a first look at August arrivals, with preliminary data indicating a continued increase from July, though we anticipate the estimate to decline but are waiting for further evidence. July’s import estimate still suggests a rebound, albeit this week’s estimate points to a lower level. Finally, domestic production jumped up after two consecutive weeks of retreating, rising to just below the post-pandemic average.

HRC Spot Prices – US Domestic & Global

- The global HRC spot price declined to $666 from $661. This dip was mainly due to a -$26 in Russia, and a -$10 in

- The Domestic – Global HRC spread expanded further, widening from -$1.44 to $19.45, flipping positive after remaining negative for six weeks.

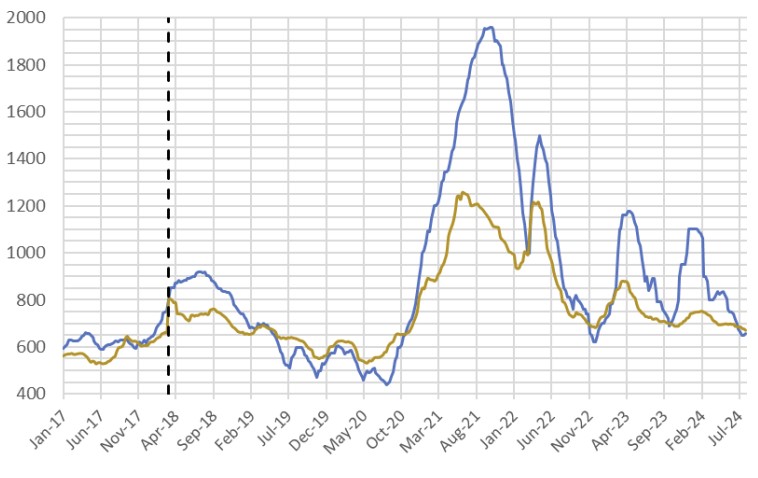

Total Sheet Imports (s.ton)

- This week’s imports estimated sheet arrivals for August indicate an increase from July’s rebounding, rising to 924k tons from July’s preliminary estimated figure of 888k.

- Given the current negative differential, it is highly unlikely that we would see another surge in arrivals for the remainder of the year. That said, we do anticipate some volatility in these figures as we push below the longer run “neutral level”.

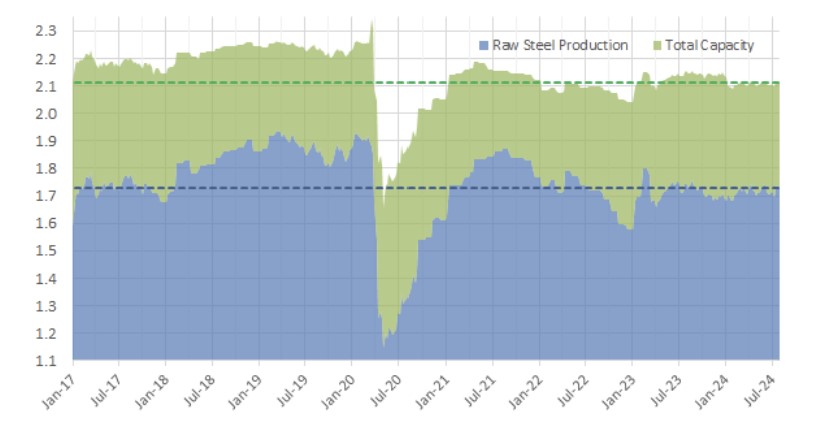

Domestic Production (s.ton)

- For the week ending on August 10th, capacity utilization ticked up by 0.6% to 78.1% and domestic raw steel production climbed to 1.735m from 1.722m/tpw.

- This brings the year-to-date production to 54.156m, operating at a rate of 5%, -2.1% below this point last year.