Supply Tracker

Key Takeaway:

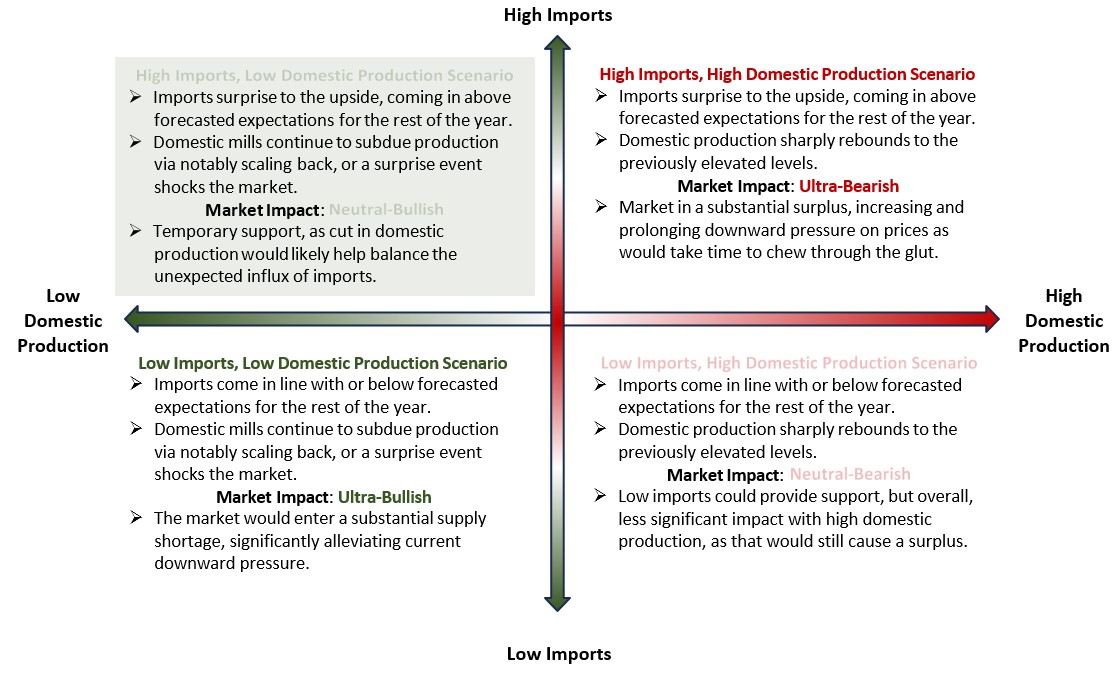

The supply dynamics are in the High Imports, Low Domestic Production quadrant. Interestingly, the significant potential upside impact of this level of domestic production cuts is currently offset by the unexpected surge in import arrivals on a ton-by-ton basis.

Current Situation:

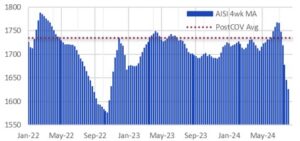

Domestic steel production eased to its lowest level since December 2022 in early October. While it has rebounded slightly, production remains subdued after being elevated for the past few months, where it peaked in August at the highest level since February 2023. The significant cuts in production coincide with the planned outage season, but unlike last year – when similar tonnage was announced – mills do not appear to be ramping up at active facilities to offset maintenance.

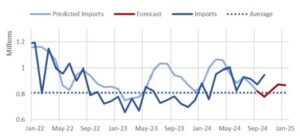

Steel imports, on the other hand, are taking longer than anticipated to ease off May’s two year high. The preliminary September data estimate shows arrivals at their lowest since February, but preliminary figures for October arrivals indicate a sharp increase, reaching the highest level since the recent May peak. This surge is exceeding expectations, driven largely by a flood of imports from Vietnam and Taiwan, in a potential attempt to bring in corrosion resistant products before the trade case is decided.

Looking Forward:

If domestic steel production remains subdued, this could provide notable upward pressure on steel prices, skewing risk to the upside, since domestic production accounts for nearly 80% of steel in the U.S. domestic market. Another factor limiting the near-term impact of reduced domestic production is the currently high levels of downstream inventory that will need to be depleted.

*The impact on the market is subject to the magnitude in which these scenarios would occur, along with the fact that domestic production is the vast majority of US steel supply.