Macro Flash Report

Consumer Price Index (CPI)

Takeaway: November’s CPI print came in line with expectations but continues to show stubborn stickiness in prices. While next week’s FOMC rate cut appears all but confirmed, we anticipate a significant change in the FOMC’s projection for next years cuts.

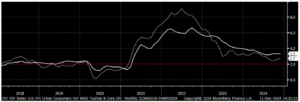

CPI YoY – Topline (dotted) & Core (solid)

In November, the Core (Ex Food & Energy) CPI YoY held steady for the third consecutive month, meeting market expectations of 3.3%.

- The shelter index (4.7% vs 4.9%) and transportation services (7.1% vs 2%) experienced softer increases.

On a monthly basis, Core CPI also come in line with forecasts and remained unchanged for the fourth consecutive month at 0.3%.

- The shelter index eased (0.3% vs 4%) yet accounted for nearly 40% of the overall advance.

The topline CPI YoY met the anticipated tick up to 2.7% from 2.6% in October, marking the second consecutive month of increases and the highest level since July. However, it is important to note that this rise is partly influenced by low base effects from last year.

- Energy costs declined less (-3.2% vs -4.9%), while food accelerated (2.4% vs 2.1%).

On a monthly basis, CPI also come in line with forecasts, rising to 0.3% from 0.2% in the previous month. This marks the highest rate since April.

- Food prices (0.4% vs 2%) and energy (0.2% vs 0.0%) both rose.

Looking forward, the November data solidified expectations for a rate cut by the Fed next week, as the probability of a December 25 basis point cut increased to 94.7% from an 88.9% probability the day prior.