Fundamental Report

Supply-Side Takeaway:

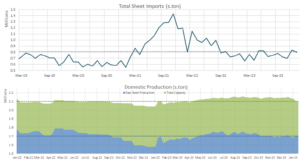

US domestic production and Imports, although slightly down on the week, continued to indicate that supply will trend higher over the quarter, putting downward pressure on steel prices.

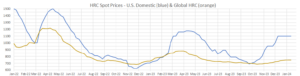

The spread between Domestic – Global prices remained stable, as gains in Europe and Turkey were offset by declines in other watched global markets, most notably in China and Russia, which experienced the largest price decreases. Imports for January, although dipping slightly compared to December, are trending higher. Furthermore, despite a slight reduction from the significant uptick last week, US domestic capacity utilization is clearly trending higher and is out of its previous subdued state, which suggests that mills are sustaining increased supply to capitalize on the remaining high profit margins.

Notes:

- The global HRC spot price stayed at $747, with $20 increase in Europe and Turkey’s $17 rise being neutralized by a $10 decrease from China, -$9 from Brazil, and -$11 from Russia.

- The Domestic – Global HRC spread remained at $353, continuing to be just below the peak spread of $356 in May 2022.

- Estimated arrivals for January are at 800k, slightly down from December’s estimated arrivals of 863k.

- For the week ending on January 13th, capacity utilization ticked down by 4% to 76.5%, bringing domestic raw steel production down to 1.699m net tons.